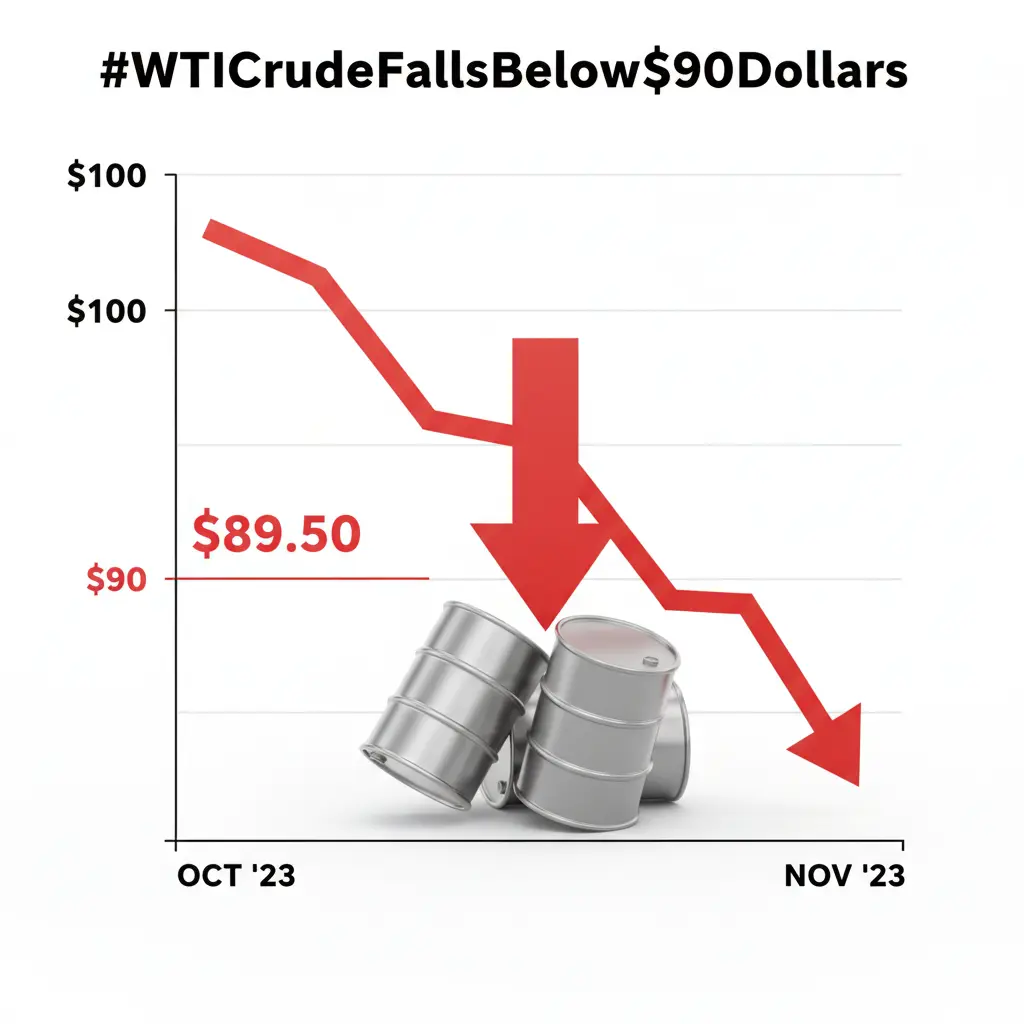

#WTI原油失守90美元 #TradFi交易分享挑战 Oil Prices: Expectations of US-Iran Agreement Suppress Prices, Downstream Demand Under Pressure

Opening Conclusion

This week, international oil prices declined significantly due to changes in geopolitical expectations, and global crude oil demand forecasts have also been adjusted. The downstream chemical markets showed mixed performance, with polyethylene prices following oil prices downward, while polypropylene maintained some support due to its unique supply and demand structure.

Why It’s Worth Watching Now

Crude oil, as the mother of global commodities, not only directly influences energy costs through its price fluctuations but also transmits through the industrial chain to downstream chemical markets, affecting macroeconomics. Currently, the evolution of geopolitical situations and the pace of global economic recovery jointly constitute key variables in oil price trends. A detailed review of this week’s oil prices and downstream market changes helps us understand the main driving factors of the current market and provides reference for future investment decisions.

Three Key Observations

1. What Changed This Week: Oil Prices Fell Sharply Due to Agreement Expectations, Downstream Polyethylene Under Pressure

This week, international oil prices experienced a sharp correction. According to Haitong Futures’ research report “Oil Futures Strategy Outlook for June 2026: Agreement Expected, Slow Downward Shift in Focus,” Brent crude oil once peaked at $115.3 per barrel in May, then fell sharply due to the expectation that the US-Iran memorandum might be reached. The progress of this geopolitical event increased market expectations of increased oil supply, thereby lowering the price focus.

Meanwhile, global crude oil demand expectations were also revised downward. Haitong Futures pointed out that the global crude oil demand forecast for Q2 2026 was lowered by 0.9 million barrels per day to 14.3k barrels per day, further intensifying downward pressure on prices. Driven by the significant decline in international oil prices and fundamental factors, the downstream polyethylene market prices overall retreated. Hongye Futures’ report “Polyethylene: Supply and Demand Gap Widens, Prices Fall” noted that domestic polyethylene spot prices fell overall this week, with weekly declines of 49-351 yuan/ton. The overall operating rate of downstream terminals remained at 36.28%, with both agricultural film and packaging film operating rates weakening simultaneously. Cautious procurement sentiment indicated demand weakness.

2. What Has Not Changed: Polypropylene Spot Tightness Remains Unresolved, Low Inventory Supports Prices

Despite the sharp decline in international oil prices, the polypropylene market showed some resilience. According to Hongye Futures’ report “Polypropylene: Falling Prices, Spot Support,” this week’s domestic polypropylene production was 681.6k tons, an increase of 14.3k tons from the previous period. However, the increase in May was below expectations, so the tight spot situation has not been fundamentally alleviated. More importantly, polypropylene commercial inventory was 634.1k tons, down 8,740 tons month-on-month, with inventories at production enterprises and traders decreasing in tandem. Low inventory levels provided strong support for spot prices.

This indicates that, although macro oil prices are under pressure, polypropylene’s supply and demand structure—especially low inventory—allows it to resist some downward pressure in the short term, and the spot market continues to maintain a support stance.

3. What to Watch for Next Week: Progress of US-Iran Agreement and Off-Season Downstream Demand

Looking ahead to next week, market focus will be on the further development of the US-Iran agreement. If the agreement is reached and implemented as expected, crude oil supply will likely face further easing expectations, and the price focus may continue to shift downward. Conversely, if progress is hindered or uncertainties arise, oil prices could receive short-term support.

At the same time, downstream demand performance is also crucial. For polyethylene, as the downstream enters the traditional off-season, whether terminal operating rates and procurement willingness can improve will directly impact price trends. For polypropylene, whether low inventory can continue to support spot prices and how new capacity releases will influence the market are key factors to watch next week.

Risks and Divergences

The main risks currently facing the market include: evolving geopolitical conflicts potentially causing new shocks to oil supply; a slowdown in global economic growth further suppressing crude demand; and whether the US-Iran agreement can be successfully reached and its market impact. Additionally, in the traditional off-season, weaker-than-expected demand recovery in downstream chemical markets may also exert downward pressure on prices.

This content is for informational sharing only and does not constitute investment advice.

$XTIUSD $XBRUSD