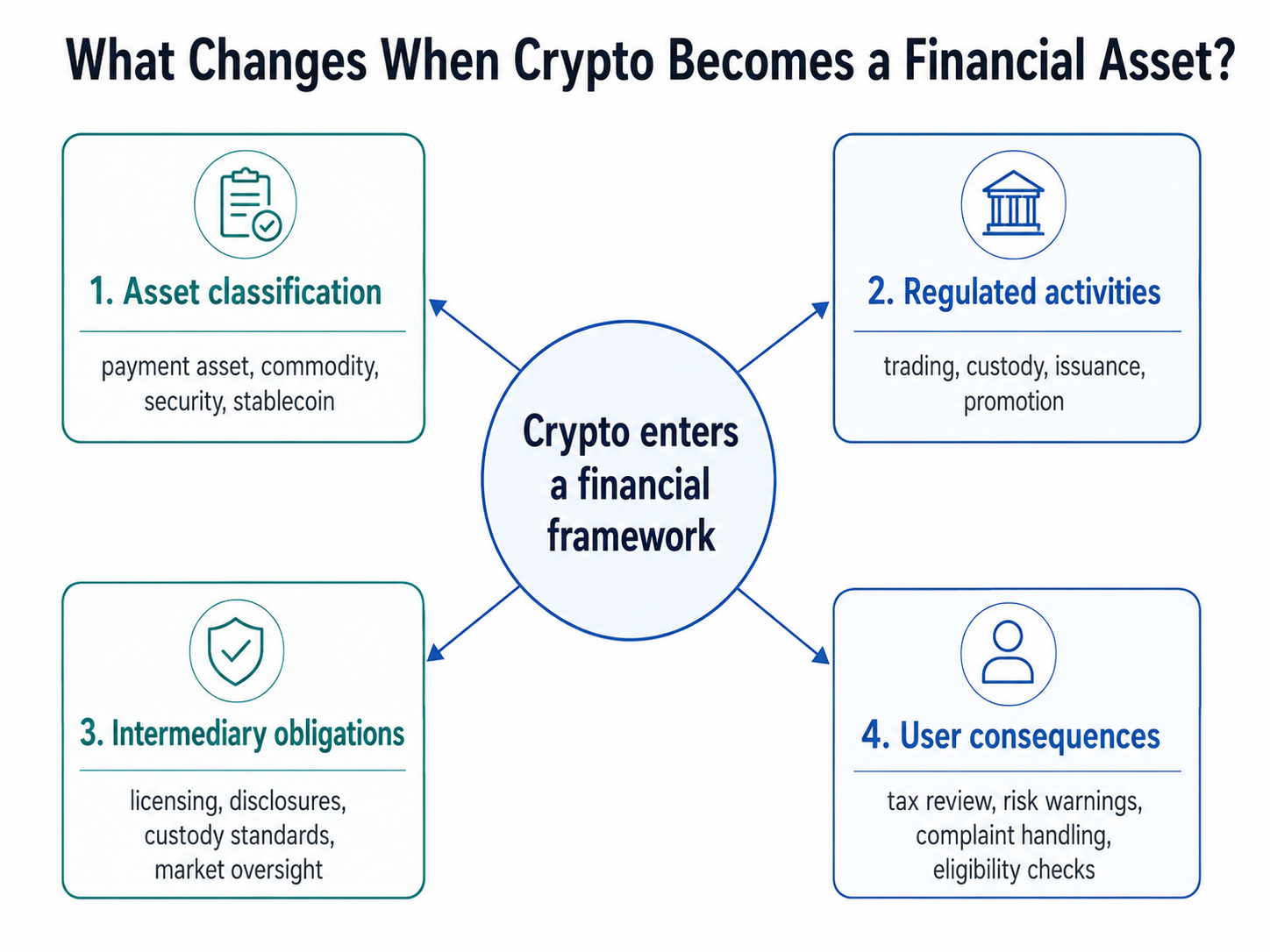

When crypto becomes a financial asset, a government begins treating certain crypto assets or crypto-related activities as part of its formal financial system. The change can bring trading, custody, issuance, promotion, or management of those assets within established financial laws.

The exact consequences depend on the jurisdiction. “Financial asset” is not a universal crypto category with identical rules everywhere. One country may use it as a broad regulatory concept, while another separates crypto into payment tokens, commodities, securities, stablecoins, or digital collectibles.

The key point is that legal treatment usually follows the asset’s rights and use, not the fact that it exists on a blockchain. A tokenized bond, payment token, governance token, and digital collectible can therefore face different rules.

What Is a Financial Asset?

A financial asset is an economically valuable right, claim, or interest recognized within a financial or legal system. Traditional examples include shares, bonds, bank deposits, fund units, and derivatives.

Crypto does not always fit these established categories. Some tokens provide access to software, some support payments, and others represent ownership, debt, income, or contractual rights. This is why regulators increasingly examine what a crypto asset does and what its holder is entitled to receive.

Blockchain technology does not determine the legal category by itself. Recording an asset on-chain can change how ownership or transfers are managed, but it does not erase the legal character of the underlying claim.

For example, a tokenized bond remains connected to debt and repayment rights. Understanding how real-world assets are tokenized shows why the legal structure behind a token can be as important as its smart contract.

What Actually Changes?

A useful way to understand reclassification is to examine four separate questions.

| Area |

Central Question |

Possible Effect |

| Asset |

What rights does the token represent? |

Classification as a payment asset, commodity, security, stablecoin, or another category |

| Activity |

What is being done with it? |

Rules for issuing, trading, promoting, staking, advising, or custody |

| Intermediary |

Who provides the service? |

Licensing, governance, capital, recordkeeping, or asset-segregation requirements |

| User |

What protections and duties apply? |

Disclosures, complaint procedures, tax reporting, eligibility checks, and risk warnings |

This framework prevents a common mistake: assuming that one label creates the same outcome for every token and transaction.

In the United Kingdom, for instance, the Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2026 brought a broader range of crypto activities within the Financial Conduct Authority’s future regulatory perimeter. Firms performing covered activities will require authorization when the expanded regime takes effect on October 25, 2027.

The rules affect activities and service providers, not only the digital asset considered in isolation.

Does Financial-Asset Status Make Crypto a Security?

No. A financial asset is a broad concept, while a security is a more specific legal category that commonly includes shares, bonds, notes, and investment contracts.

A crypto asset may represent a security, but many do not. The US Securities and Exchange Commission’s March 2026 interpretation distinguishes digital securities from categories including digital commodities, digital collectibles, digital tools, and certain stablecoins. It also explains that a non-security crypto asset may still become subject to securities law when offered or sold as part of an investment contract.

This means three questions may produce different answers:

-

Is the token itself a security?

-

Was it sold through a securities transaction?

-

Does a service involving it fall under another financial law?

A token’s name, ticker, price, or blockchain cannot answer these questions alone. Regulators may examine its embedded rights, distribution, marketing, issuer promises, network function, and transaction structure.

A Practical Example

Assume a country previously supervised crypto platforms mainly for anti-money laundering compliance. It then introduces a financial-services regime covering crypto trading and custody.

The blockchain does not change. Users may still deposit assets and place orders in much the same way. Behind the interface, however, the platform may need financial authorization, customer-asset segregation, stronger governance, market-abuse monitoring, capital resources, and standardized disclosures.

Users may gain clearer information about who holds their assets, what happens during insolvency, how complaints are handled, and which regulator supervises the provider.

However, these protections do not guarantee repayment or prevent losses. Regulation can reduce certain conduct and operational risks, but it cannot eliminate volatility, hacking, fraud, smart contract failures, or provider insolvency.

Can the Classification Change Crypto Taxes?

It can influence tax policy, but regulatory and tax classification are separate decisions.

A government may treat crypto as a financial asset under market law while continuing to tax disposals as property gains, miscellaneous income, business income, or another category. Reclassification therefore does not automatically establish a new tax rate or reporting method.

Users should verify four points independently:

-

which transactions create a taxable event;

-

how gains and losses are calculated;

-

whether income from staking or lending has separate treatment;

-

when reporting obligations begin.

Headlines about financial recognition should not be interpreted as confirmation that tax legislation has already changed.

Benefits, Limits, and Misconceptions

Formal classification can clarify which regulator is responsible, which providers need authorization, and which disclosures or custody standards apply. Greater legal certainty may also make it easier for banks, asset managers, payment providers, and custodians to determine which crypto services they can offer.

The trade-off is that compliance can become more complex and expensive. Some providers may restrict products, customers, or jurisdictions. Cross-border differences can also create situations where the same token receives different treatment in different countries.

Most importantly, becoming a financial asset does not make crypto legal tender, eliminate risk, guarantee government protection, or convert every token into a regulated security.

Summary

When crypto becomes a financial asset, certain assets or activities enter a more formal financial framework. The change can affect classification, licensing, custody, disclosures, market conduct, institutional participation, consumer protection, and potentially taxation.

The correct follow-up question is not simply, “Is crypto now a financial asset?” It is: Which asset, activity, provider, user, and jurisdiction does the rule cover?

Those five details determine what the classification changes in practice.

FAQs

Does financial-asset status make crypto legal tender?

No. Legal tender is officially recognized money that must be accepted in specified circumstances under national law. Crypto can enter a financial regulatory framework without becoming a country’s official currency.

Not automatically. Regulation depends on the platform’s activities, location, customers, and supported assets. Some businesses may require authorization, while others may remain outside a particular regime or fall under separate rules.

Can the same token have different classifications?

Yes. Different jurisdictions may classify the same token differently. Its treatment can also depend on whether the issue concerns the token itself, the way it was sold, or a service involving it.

Is a tokenized stock still a security?

A token that legally represents a stock or comparable equity right will generally retain the characteristics of a security. The blockchain changes the method of representation or recordkeeping, not necessarily the underlying legal rights.

Does regulation make crypto safe?

No. Regulation may improve disclosures, custody practices, governance, and oversight, but it cannot remove market volatility, cyberattacks, fraud, operational failure, or smart contract risk.