Over the past decade or more, the digital asset market has earned a reputation for openness and innovation, but it has also seen recurring problems like exchange bankruptcies, user asset losses, stablecoin risks, and market manipulation. MiCA emerged against this backdrop, designed to create a unified regulatory framework for crypto assets across Europe.

For exchanges, stablecoin issuers, and Web3 companies, MiCA means higher compliance standards. For everyday investors, the impact is even more direct—whether it's opening an account, buying crypto, using stablecoins, or handling asset custody and cross-platform transfers, everything will be shaped by MiCA's regulatory framework.

Will MiCA Restrict Ordinary Users from Buying and Selling Crypto?

Many investors want to know: Will MiCA limit their ability to buy Bitcoin or other cryptocurrencies?

The short answer is no. MiCA's core mission is to regulate the market, not to ban user participation. Everyday users can still buy Bitcoin (BTC), Ethereum (ETH), and other compliant digital assets.

What does change is the trading environment. Going forward, users are more likely to trade through CASP-authorized licensed exchanges, rather than through unregulated platforms. That means greater market transparency and stronger customer protection obligations for exchanges.

For most users, the act of trading itself won't change fundamentally, but the market environment will become more regulated.

User Trading Environment: Before vs. After MiCA

| Item |

Before MiCA |

After MiCA |

| Trade cryptocurrencies |

Freely tradable |

Freely tradable |

| Bitcoin (BTC) purchase |

Supported |

Supported |

| Ethereum (ETH) purchase |

Supported |

Supported |

| Exchange regulatory standards |

Varies by country |

Unified EU standards |

| Investor protection |

Platform-dependent |

Unified regulatory requirements |

| Risk disclosure |

Inconsistent |

Mandatory disclosure |

| User asset protection |

Determined by platform |

Unified under MiCA |

For ordinary investors, MiCA doesn't restrict crypto trading—it improves market transparency and user protection through a unified regulatory framework.

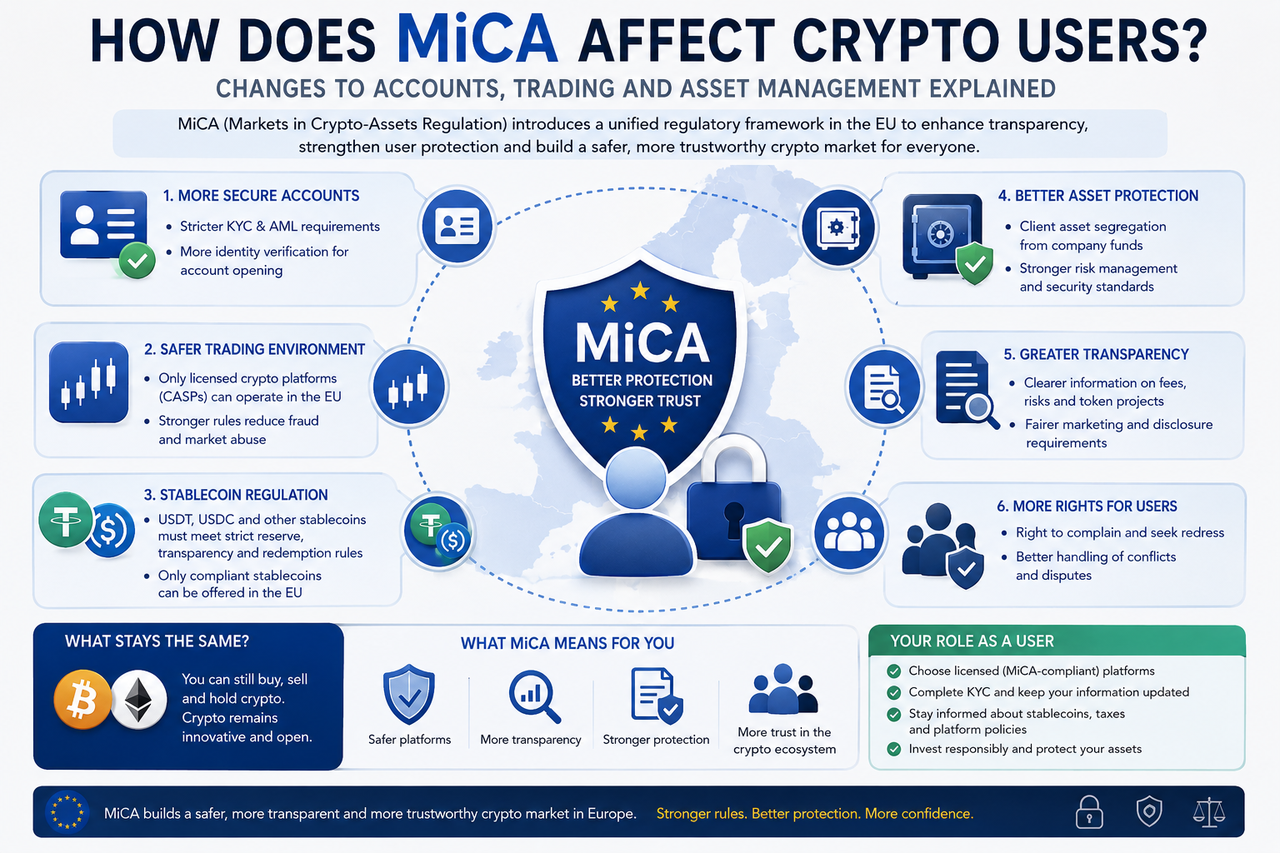

Will MiCA Make Account Registration and KYC Verification Stricter?

This is one of the most noticeable changes MiCA brings.

With the full rollout of the CASP regime, licensed exchanges must comply with stricter Anti-Money Laundering (AML) and Know Your Customer (KYC) rules. As a result, users may need to submit more complete identity information and verification documents when opening accounts.

Some platforms may also require proof of address, source of funds explanations, or additional identity verification steps to meet regulatory standards. While this adds complexity to onboarding, stricter identity checks help reduce money laundering, fraud, and illegal fund flows, ultimately strengthening trust in the entire industry.

Most Noticeable MiCA Changes for Ordinary Users

| User Activity |

Before MiCA |

After MiCA |

| Register exchange account |

Some platforms have low requirements |

Stricter identity verification |

| KYC authentication |

Standards vary across platforms |

Unified higher verification requirements |

| Address proof |

Some platforms don't require it |

Required in some cases |

| Large transaction review |

Rare |

Stricter |

| AML checks |

Platform-driven |

Mandatory |

| User data updates |

Irregular |

More periodic reviews |

| User asset protection |

Platform-determined |

Unified under MiCA |

For ordinary users, the account setup process may become slightly more involved, but the payoff is greater security and lower compliance risk.

Will MiCA Affect the Use of USDT and USDC?

Stablecoins like USDT and USDC are a key focus area for MiCA.

Under MiCA, stablecoins are classified into two categories: E-Money Tokens (EMTs) and Asset-Referenced Tokens (ARTs). Issuers must meet requirements for reserve management, disclosure, and user redemption rights.

The biggest change for ordinary users is likely the range of stablecoins available on exchanges. Some stablecoins that don't meet MiCA requirements may face restrictions, while compliant ones will find it easier to access the European market.

Over the long term, this regulatory framework boosts stablecoin transparency and security, reducing market risks tied to reserve asset issues.

Will MiCA Make User Assets Safer?

Investor protection is a core goal of MiCA.

In recent years, the crypto industry has seen several platform bankruptcies and customer asset losses. Many cases show that a lack of regulation and internal controls is often the root cause. That's why MiCA requires licensed exchanges to implement customer asset segregation, ensuring user funds are kept separate from the platform's own assets. Companies must also establish risk control systems, information security mechanisms, and emergency response plans.

While these measures can't eliminate investment risk entirely, they can significantly reduce the impact of platform operational risks on user assets.

Key Safeguards MiCA Provides to Users

| Regulatory Requirement |

Protection for Users |

| Customer asset segregation |

Reduces risk of platform misusing user funds |

| Risk management framework |

Improves exchange operational stability |

| Cybersecurity requirements |

Reduces risk of hacking attacks |

| Disclosure obligations |

Increases project transparency |

| Stablecoin reserve regulation |

Reduces de-pegging risk |

| Ongoing regulatory oversight |

Prevents non-compliant practices |

| Complaint handling mechanism |

Clearer channels for user recourse |

These measures can't eliminate investment risks from market volatility, but they can significantly lower the risk of asset losses caused by platform operational issues.

Will MiCA Change the Trading Experience for Users?

For most users, the trading interface and process won't change noticeably. You can still trade spot, set up recurring buys, convert assets, and participate in the market as before.

However, platforms will face stricter oversight on product listings, token issuances, and risk disclosures. In the future, you may see more detailed information about project risks, token mechanisms, and market data—helping you make better-informed investment decisions.

While this increases the information disclosure burden on platforms, it also helps investors make more rational choices.

Will MiCA Affect Decentralized Finance (DeFi)?

Currently, MiCA primarily regulates centralized service providers.

For fully decentralized DeFi protocols with no central operating entity, MiCA doesn't provide a complete regulatory framework. But if a DeFi project is actually run by a specific team or serves European users through centralized platforms, those activities may still face regulatory scrutiny.

For ordinary users, most DeFi products remain accessible, but European regulators may refine the rules further in the future.

Will MiCA Raise the Barrier to Entry for Crypto Investment?

From a technical standpoint, MiCA doesn't set a minimum investment amount or ban retail investors from the digital asset market.

That said, because account verification is stricter and platform operations are more regulated, some users may feel the barrier to entry has increased. This shift essentially mirrors the regulatory model of traditional financial markets: investors need to complete identity verification and trade through compliant platforms, rather than using any unregulated platform freely.

In the long term, this mechanism helps improve market stability and investor confidence.

Will MiCA Make Cryptocurrency Taxation More Transparent?

While MiCA itself isn't a tax law, the unified regulatory framework will make digital asset activities more transparent.

Licensed entities must maintain transaction records and comply with regulatory reporting requirements. As the EU pushes forward with the Crypto Asset Tax Information Sharing mechanism, cross-border digital asset transactions are likely to become more transparent.

For ordinary users, this means more standardized tax reporting and asset management, and investors will need to pay closer attention to their own compliance obligations.

MiCA raises the industry's barrier to entry, meaning some platforms won't be able to meet the new regulatory standards.

Going forward, the European market will be increasingly dominated by platforms with CASP authorization, while smaller platforms lacking compliance capabilities may exit or relocate to other regions. For users, this means fewer platform choices but higher overall quality and security.

From a long-term perspective, market consolidation often leads to a more mature and stable industry ecosystem.

How Will MiCA Change the European Cryptocurrency Market?

MiCA's implementation marks a new chapter for Europe's digital asset industry.

In the past, the market was driven mainly by innovation. Now, it will strike a balance between innovation and regulation. Large exchanges, stablecoin issuers, and traditional financial institutions will find it easier to enter the market, while institutional investor participation is expected to keep rising.

For ordinary users, this means access to a more regulated, secure, and transparent digital asset service system. Some processes will become stricter, but overall user protection will also improve.

Conclusion

MiCA will not ban ordinary users from buying or holding cryptocurrencies, but it will fundamentally change how they engage with the market. Account registration will be more standardized, KYC verification will be stricter, stablecoin issuance will face unified oversight, and exchanges will need to build more robust customer asset protection mechanisms.

In the short term, some users may need to adjust to new compliance requirements. In the long term, MiCA will enhance market transparency, strengthen asset security, and push Europe's crypto industry toward greater maturity and institutionalization.

FAQs

Will MiCA Ban Ordinary Users from Buying Bitcoin?

No. MiCA will not ban users from buying, holding, or trading mainstream cryptocurrencies like Bitcoin and Ethereum. Its primary goal is to regulate market participants.

Will MiCA Make Account Registration More Complicated?

To some extent. Exchanges must follow stricter KYC and AML rules, so users may need to provide more identity verification materials.

Will MiCA Affect USDT and USDC?

Yes. MiCA sets up a dedicated regulatory framework for stablecoins, requiring issuers to meet reserve management, disclosure, and redemption mechanism requirements.

Can MiCA Protect User Assets?

MiCA requires licensed entities to implement customer asset segregation and risk management systems, which can improve user asset security, but it cannot eliminate all market risks.

What Preparations Do Ordinary Users Need to Make for MiCA?

Users should prioritize licensed exchanges, complete necessary identity verification, and keep an eye on changes in stablecoins, taxation, and platform compliance policies to adapt to the new regulatory environment.