Summary

-

In May 2026, global markets repeatedly shifted between geopolitical disruptions, policy expectations, and the recovery of risk appetite. The cryptocurrency market as a whole entered a volatile phase characterized primarily by structural opportunities.

-

ETF inflows slowed significantly and temporarily turned into net outflows, reflecting a shift in institutional capital from active allocation to cautious observation, while the market lacked a unified short-term direction.

-

Global equity markets generally continued to rise. U.S. stocks remained strong, driven by the AI theme, with semiconductor and healthcare sectors leading the gains. Overall sentiment toward risk assets improved.

-

Gold traded sideways at elevated levels, while oil prices dominated commodity market volatility, indicating that safe-haven demand has not completely faded. Global macro pricing remains influenced by geopolitical risks and inflation expectations.

-

Prediction markets and crypto payment cards continued to expand, with the industry’s focus gradually shifting from trading narratives toward compliance, payment applications, and infrastructure driven by real revenue generation.

-

Gate officially launched stock trading, allowing users to directly trade stocks, ETFs, and other assets listed on major U.S. securities markets using USDT on the platform.

1. Macroeconomic Market Trends

1.1 Recurring Geopolitical Tensions Continue to Pressure Global Risk Appetite

The dominant macro theme in May remained the repeated disruptions caused by geopolitical events. Although the Middle East situation briefly showed signs of ceasefires and progress in negotiations during the month, overall developments remained unstable. Localized conflicts and repeated implementation setbacks prevented markets from fully pricing out related risks. Similarly, the Russia–Ukraine conflict saw short-lived attempts at de-escalation, but these lacked sustainability, indicating that global political uncertainty remained elevated.

Against this backdrop, safe-haven sentiment periodically strengthened, supporting assets such as crude oil and gold, while global risk assets generally adopted a more cautious tone.

For the cryptocurrency market, the external environment in May was far from favorable. Rising geopolitical risks tend to suppress overall market risk appetite, driving capital toward defensive assets such as cash and gold. Highly volatile crypto assets are more susceptible to sentiment-driven fluctuations, resulting in amplified short-term price volatility. Structurally, Bitcoin generally remained more resilient due to its liquidity and broad market consensus, whereas altcoins and high-volatility sectors were more vulnerable when risk appetite weakened.

As a result, the crypto market in May was largely characterized by competition among existing capital rather than fresh inflows. Market activity was driven mainly by defensive positioning, cautious observation, and event-driven trading. A broad-based rally is unlikely until external uncertainties decline further.

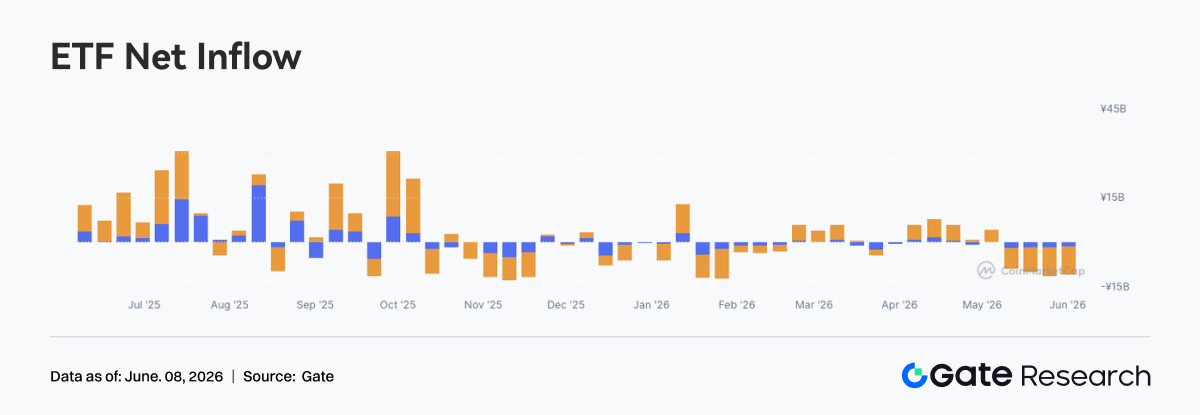

1.2 ETF Flows: ETF Inflows Slowed Significantly as Market Sentiment Turned More Cautious

In May 2026, the cryptocurrency ETF market generally displayed slower capital inflows and increasing net outflows. In conjunction with market performance, the gradual decline in Bitcoin and Ethereum prices during the month led to a noticeable reduction in investor risk appetite. Institutional capital shifted from active allocation to a more cautious wait-and-see approach.

Compared with the sustained inflows seen during the second half of 2025 and the beginning of 2026, ETF fund flows cooled significantly in May, reflecting the market's lack of a clear short-term directional outlook.

From a structural perspective, spot Bitcoin ETFs remained the primary driver of overall fund flows. During May, Bitcoin continued to retrace after consolidating at elevated levels, prompting some institutional investors to lock in profits and reduce risk exposure. Toward month-end, ETF net outflows expanded further, coinciding with Bitcoin’s break below key support levels. This reflected a gradual shift in sentiment from optimism to caution.

The increase in outflows also indicated growing concerns among institutional investors regarding short-term market volatility.

At the same time, spot Ethereum ETFs also experienced relatively weak fund performance. Although Ethereum’s ecosystem and long-term growth prospects continued to attract market attention, the broader market correction dampened demand for new capital allocation, resulting in a notable decline in ETF liquidity.

Overall, the cryptocurrency ETF market exhibited a net outflow trend in May. Institutional asset allocation became more conservative, and the market entered a phase of adjustment. In the short term, investors appeared more inclined to wait for greater clarity regarding the macro environment and market sentiment before making large-scale allocations.

1.3 Global Capital Market Trends

1.3.1 Major Global Equity Indices: Rising Risk Appetite Drives Continued Gains in U.S. Stocks

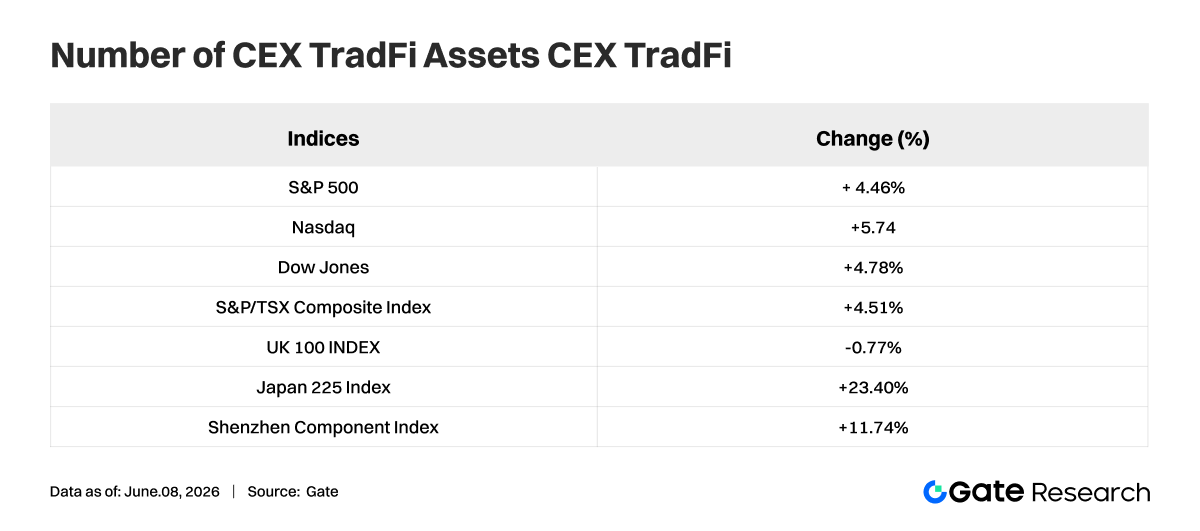

In May 2026, major global equity indices generally maintained their upward momentum, with the U.S. market standing out in particular. The Nasdaq Composite Index rose 5.61% during the month, the S&P 500 gained 4.39%, and the Dow Jones Industrial Average increased 4.77%, reflecting strong market confidence in U.S. economic growth prospects and corporate earnings. The technology sector continued to serve as a key driver of market gains.

Among other major markets, Canada’s S&P/TSX Composite Index rose 4.60%, largely in line with the performance of U.S. equities. In contrast, the UK FTSE 100 Index declined slightly by 0.26%, showing relatively weak performance. Meanwhile, the VIX Volatility Index, a widely used measure of market fear, fell 12.70% during the month, indicating improved investor risk appetite and a noticeable decline in demand for safe-haven assets.

Overall, global equity markets demonstrated considerable resilience in May 2026, with most major economies posting positive returns. Risk assets outperformed safe-haven assets, and overall market sentiment remained optimistic, providing a favorable environment for global capital markets. However, as valuations continue to rise, investors should remain attentive to the potential impact of macroeconomic data, monetary policy changes, and geopolitical developments.

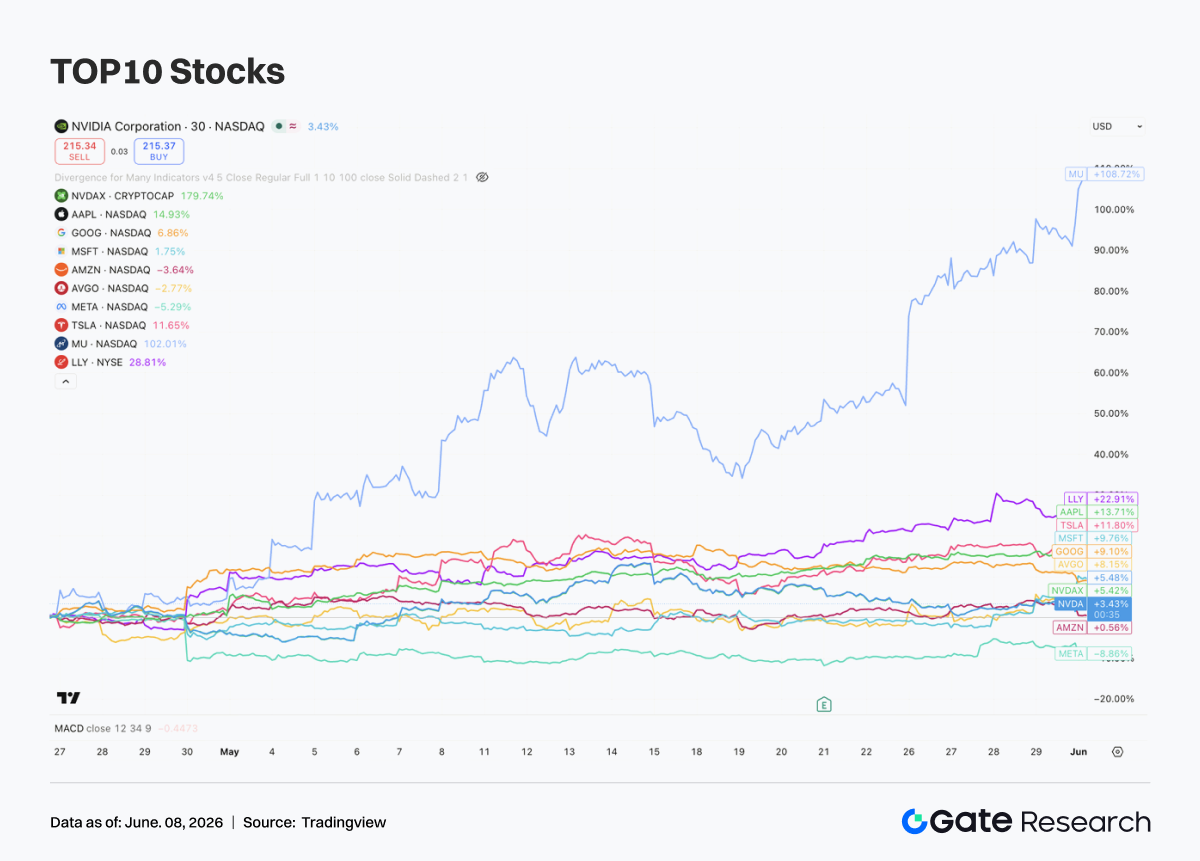

1.3.2 Equities: The AI Theme Continues to Strengthen, While Semiconductors and Healthcare Lead the Market

In May, the ten largest U.S. companies by market capitalization generally continued their upward trend, although divergence among sectors and individual stocks became increasingly pronounced. The dominant market theme remained artificial intelligence, with capital continuing to concentrate in industry leaders possessing AI infrastructure, cloud computing capabilities, and highly visible earnings growth.

The semiconductor sector clearly led the market. Expectations for growing AI computing demand continued to rise, driving valuation expansion across the entire semiconductor supply chain. Among these companies, Micron Technology (MU) delivered the strongest performance, benefiting from surging demand for HBM (High Bandwidth Memory) and continued data center expansion, resulting in a doubling of its share price. Although NVIDIA (NVDA) posted relatively more moderate gains, it remained resilient despite already having experienced substantial appreciation over the previous two years.

At the same time, companies such as Broadcom (AVGO), which provide networking and custom chip solutions, also continued to benefit from the AI infrastructure investment cycle. This suggests that capital has expanded beyond a singular focus on GPUs to encompass the broader AI computing ecosystem.

Healthcare emerged as another important investment theme during May. Eli Lilly (LLY) generated significant excess returns, driven by continued growth in sales of its GLP-1 weight-loss and diabetes treatments. The market increasingly views the company as a rare asset combining both technology-style growth characteristics and the defensive qualities traditionally associated with healthcare.

1.3.3 Gold: Cooling Safe-Haven Demand Leads to Consolidation at Elevated Levels

In May, international gold prices generally traded within a high-level consolidation range. Following a prolonged rally that pushed prices to record highs, the market entered a phase of profit-taking, with gold declining by approximately 0.8% during the month.

Although the magnitude of the correction was limited, it reflected investors’ reassessment of short-term safe-haven demand and expectations regarding future interest-rate cuts.

However, the long-term investment thesis for gold remains fundamentally unchanged. Continued accumulation of gold reserves by central banks, challenges to the credibility of the U.S. dollar system, and expectations for future monetary easing among major economies continue to provide medium- and long-term support for gold prices.During this correction, gold remained close to historical highs, demonstrating that market demand for gold allocation remains strong.

Overall, May’s gold market performance appeared more like a technical consolidation following a substantial rally rather than a trend reversal. Against a backdrop of slowing global economic growth, persistent geopolitical uncertainty, and increasingly accommodative monetary policies among major central banks, gold continues to possess significant strategic allocation value.

The most significant development in commodity markets during May 2026 was the re-emergence of energy prices as the primary pricing anchor across the entire market.

Repeated tensions in the Middle East, transportation risks surrounding the Strait of Hormuz, and expectations of supply disruptions led to multiple sharp rallies and selloffs in international oil prices during the month. Market sensitivity to geopolitical risk premiums increased noticeably.

According to a Reuters report published on May 12, Brent crude oil temporarily rose to approximately USD 107.77 per barrel, while WTI crude reached approximately USD 101.89 per barrel. This reflected a shift in trading logic away from concerns about demand and toward prioritizing supply security.

As a result, commodity markets in May were no longer simply tracking macroeconomic growth expectations. Instead, they became increasingly influenced by unexpected geopolitical events and the resurgence of inflation expectations. Crude oil once again emerged as a critical variable affecting global asset pricing.

Against the backdrop of oil price volatility, industrial metals displayed more differentiated performance. Metals such as copper reflected a combination of macroeconomic expectations and supply-demand dynamics. Although price elasticity remained significant, the sustainability of gains was weaker than in the energy sector.

Overall, commodity markets in May transitioned from a predominantly macro-driven trading environment into a new phase jointly driven by geopolitical shocks, interest-rate expectations, and supply constraints. Elevated volatility is likely to persist in the near term, while the dominance of energy commodities has become more pronounced relative to both precious metals and base metals.

2. Hot Sector Analysis

2.1 Prediction Markets: Institutional Inflection Point, Regulatory Trials, and Liquidity Redistribution

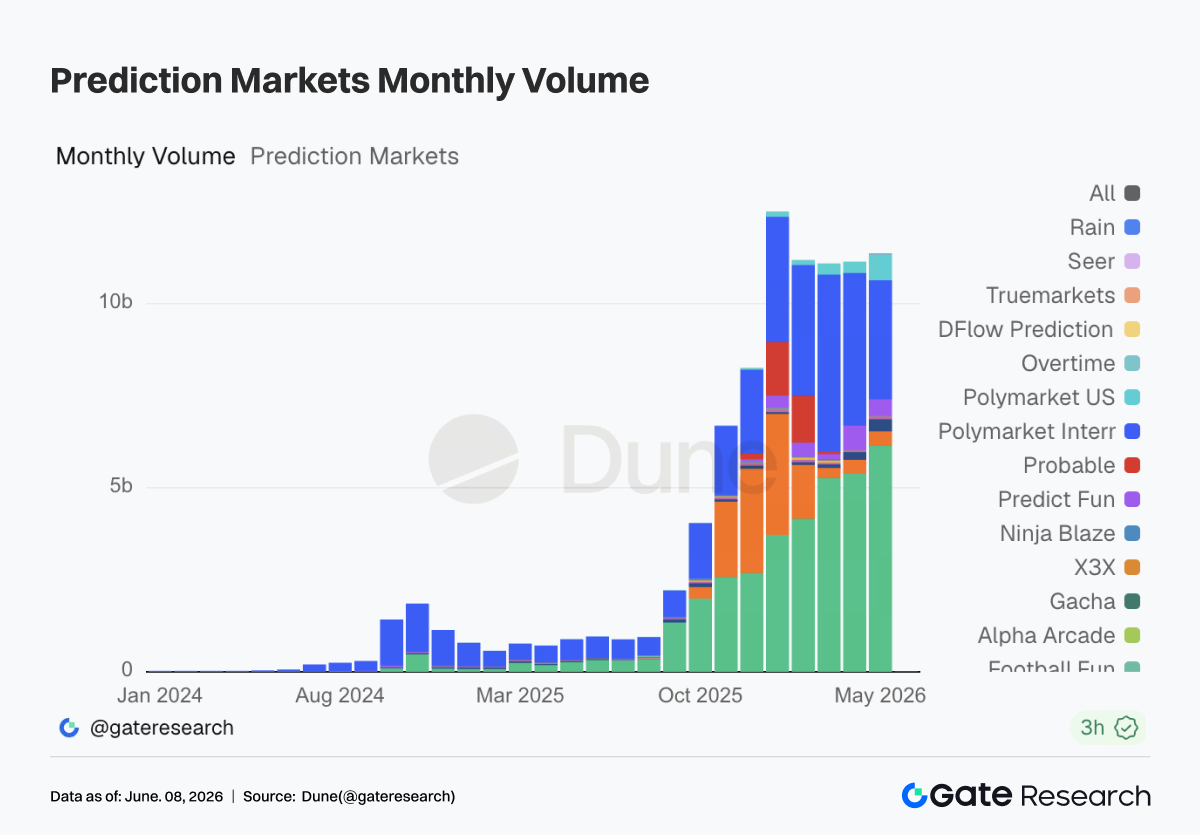

In May, prediction market taker trading volume was approximately USD 11.36 billion, a slight increase of about 2% compared with approximately USD 11.14 billion in April. Since the beginning of 2026, trading volume has remained above USD 10 billion for five consecutive months. At the same time, internal structural changes have become evident. Kalshi recorded approximately USD 6.15 billion in trading volume in May, accounting for approximately 54% of the entire market; Polymarket International recorded approximately USD 3.23 billion, accounting for approximately 28%; Polymarket US reached USD 695 million, doubling from April. Industry growth is gradually shifting from purely crypto-native traffic toward trading scenarios that are more regulated and closer to traditional derivatives markets.

In addition to trading volume itself, primary market valuations in the prediction market sector continued to grow. Kalshi completed a USD 1 billion financing round, bringing its valuation to USD 22 billion. Participants included Coatue, Sequoia, a16z, Morgan Stanley, ARK, and others. Prediction markets have already come to be viewed by mainstream capital as a type of event-risk trading infrastructure.

Kalshi explicitly stated in its fundraising materials that the capital would be used to expand services for institutional clients such as hedge funds, asset management firms, proprietary trading firms, and insurance companies, while also developing block trading, risk management products, and brokerage integrations. This is precisely the direction in which institutions are genuinely interested: transforming uncertainty related to macroeconomics, elections, policy, sports, and geopolitics into standardized contracts that can be traded, cleared, and risk-managed.

The data also supports this judgment. Kalshi’s current 30-day average daily taker trading volume is approximately USD 199 million, while its 7-day average is approximately USD 218 million. Its 7-day market share has risen to approximately 57%. Its open interest stands at approximately USD 674 million, also ranking first in the industry.

Compared with this, Polymarket still possesses strong global traffic and brand recognition. However, Polymarket International recorded approximately USD 3.23 billion in trading volume in May, lower than approximately USD 4.15 billion in April, marking two consecutive months of noticeable decline following the implementation of comprehensive fees. Meanwhile, Polymarket US increased from approximately USD 302 million in April to approximately USD 695 million in May, indicating that Polymarket’s path of returning to compliance within the United States is gaining momentum.

2.2 Crypto Payment Cards: Continuing to Move Toward Stablecoin Payment Infrastructure

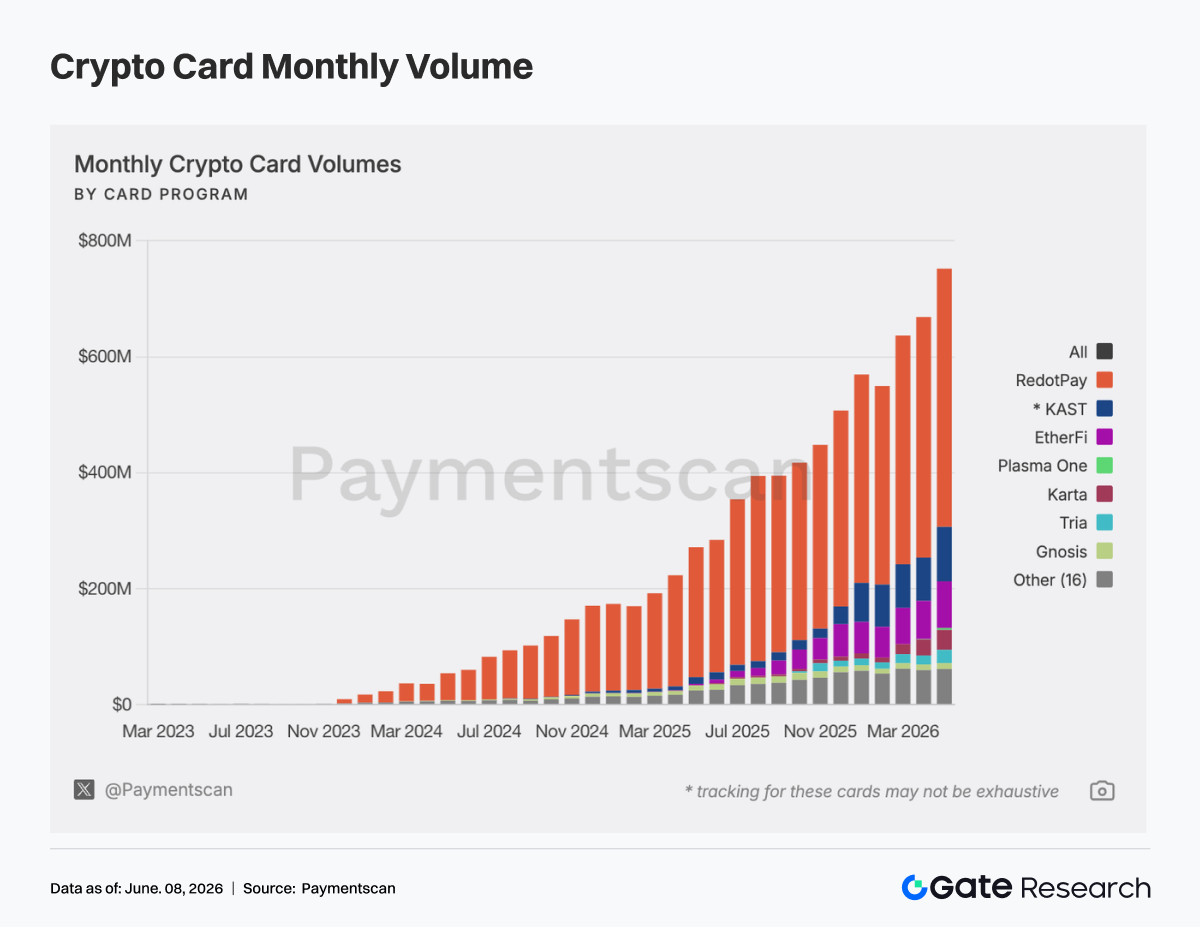

In May, crypto payment card transaction volume continued to expand. Total attributable on-chain payment card volume reached approximately USD 752 million, representing an increase of approximately 12.5% from approximately USD 669 million in April. The number of transactions reached approximately 3.05 million, up approximately 8% from approximately 2.82 million in April. The growth was not only driven by large capital inflows but also reflected more frequent real-world usage.

From the perspective of project distribution, the market remained highly concentrated in May. RedotPay recorded approximately USD 445 million in volume, accounting for approximately 59% of the entire market and maintaining an absolute leading position. KAST recorded approximately USD 93.88 million, accounting for approximately 12.5%, while EtherFi recorded approximately USD 80.40 million, accounting for approximately 10.7%. The top three projects together accounted for approximately 82% of total market volume. Although there are many crypto payment card projects in the market, only a small number of leading products have been able to establish large-scale payment or fiat on-ramp and off-ramp scenarios. This concentration indicates that clear distribution channels have already emerged within the market. Future business partnerships, card issuance cooperation, stablecoin distribution, and payment network negotiations will likely be centered around large-scale players such as RedotPay, KAST, and EtherFi.

From the perspective of daily consumer spending, RedotPay and KAST recorded average transaction values of approximately USD 766 and USD 931 respectively, suggesting a focus on large-value fiat off-ramp transactions, stablecoin off-ramping, or spending by high-net-worth users. EtherFi recorded approximately 977,000 transactions in May, with an average transaction size of approximately USD 82, making it closer to genuine everyday consumer spending. Gnosis recorded approximately 220,000 transactions with an average transaction size of approximately USD 46, while Bitget Wallet recorded approximately 450,000 transactions with an average transaction size of approximately USD 14, both displaying characteristics of small-value, high-frequency usage.

This indicates that the crypto payment card sector is gradually splitting into two business models. One consists of stablecoin cash-out cards and large-value spending cards that contribute the majority of transaction volume. The other consists of wallet-integrated daily payment cards that contribute user habits and transaction frequency.

At the blockchain level, payment card activity in May remained highly dependent on chains with deep stablecoin liquidity. Based on attributable volume by blockchain, Tron recorded approximately USD 236 million, accounting for approximately 31.5% of total chain-level volume. BSC recorded approximately USD 107 million, accounting for approximately 14.3%. Optimism recorded approximately USD 95.22 million, Solana approximately USD 91.51 million, and Ethereum approximately USD 86.01 million.

Crypto card payments are highly correlated with the stablecoin supply on each blockchain. More specifically, Tron and BSC are primarily associated with stablecoin fiat on-ramp and off-ramp activity and mass-market users, while Optimism and Ethereum are more closely related to application-oriented cards such as EtherFi. Solana reflects increasing penetration of wallet ecosystems and consumer applications.

The distribution by asset further reinforces the stablecoin payment narrative. In May, USDT accounted for approximately USD 448 million, representing approximately 61.3% of attributable volume by asset. USDC accounted for approximately USD 193 million, representing approximately 26.5%. Other assets accounted for approximately USD 67.08 million.

In essence, crypto payment cards can be viewed as a productized form of stablecoins serving as payment balances and settlement assets. In other words, stablecoins are entering real-world consumption scenarios through payment cards.

In addition, product positioning among crypto card providers is becoming increasingly differentiated. Significant differences exist among cards in terms of cashback rewards, foreign exchange fees, Apple Pay and Google Pay support, and whether borrow-to-spend functionality is available.

EtherFi focuses more on lending, yield-generating assets, and consumer spending. KAST focuses on premium stablecoin accounts and relatively high cashback rewards. Gnosis and Tria focus on low-value, high-frequency everyday payments. RedotPay functions more as a powerful off-ramp tool.

This differentiation indicates that crypto payment cards are evolving into several categories, including neobanks, wallet extensions, spending accounts linked to yield-generating assets, cross-border cash-out solutions, and regional payment gateways.

Overall, the crypto payment card market moved further toward becoming part of the broader stablecoin payment infrastructure in May. Observable monthly on-chain volume indicates that demand has already reached a meaningful scale. However, issues such as concentration among leading providers, differences in measurement methodologies, the mixing of top-up activity with actual consumption, and the absence of off-chain data still require careful consideration.

Looking ahead, three key areas deserve attention. First, whether large-value off-ramp cards such as RedotPay and KAST can continue expanding their scale. Second, whether high-frequency consumer cards such as EtherFi, Gnosis, and Bitget Wallet can improve user retention and spending per user. Third, whether card issuance and settlement infrastructure providers such as Visa, Mastercard, Rain, Wirex, Bridge, UR, Kulipa, and Immersve can successfully transform on-chain stablecoin balances into compliant, low-friction, globally accessible payment networks.

3. Industry Developments

3.1 Crypto Exchanges Launch U.S. Stock Spot Trading, Reshaping the Structure of Global Capital Markets

Between 2025 and 2026, major global cryptocurrency exchanges successively launched U.S. stock spot trading services. This trend is not accidental but rather the inevitable result of multiple forces converging.

First, the regulatory environment underwent a critical transformation. From late 2025 through the first half of 2026, the U.S. SEC and CFTC successively issued important clarifications, defining the legal status of tokenized securities and opening compliant pathways for crypto platforms. In March 2026, the SEC approved Nasdaq’s launch of tokenized Russell 1000 stocks and major ETFs. In May, the SEC further prepared to introduce an “innovation exemption” framework that would allow crypto platforms to trade tokenized versions of U.S. equities. This series of policy signals fundamentally removed the compliance constraints that had burdened the industry for many years.

In addition, cross-border investment channels have become increasingly restricted, while crypto exchanges, through USDT settlement, 24/7 service availability, and global account systems, provide users with a more convenient gateway for cross-market asset allocation.

Second, the convergence of traditional finance and crypto has become a new direction of industry competition. With the rapid development of RWAs, tokenized stocks, and on-chain traditional financial products, exchanges are transforming from single-asset crypto platforms into multi-asset financial platforms. According to CoinGecko data, spot trading volume of tokenized stocks reached USD 15.1 billion in Q1 2026, surpassing the USD 14.8 billion recorded during the entire second half of 2025. Market expansion has significantly exceeded expectations.

Third, U.S. equities continue to attract incremental global capital as they repeatedly reach new highs. The AI industry chain has made technology stocks the core investment theme of global capital markets. As the Nasdaq and S&P 500 continue setting new records, crypto exchanges have introduced stock trading services to satisfy user demand for exposure to AI, technology growth stocks, and traditional financial assets.

3.1.1 Core Differences: Tokenization vs. CFDs vs. U.S. Stock Spot Trading

Tokenized U.S. equities do not represent direct ownership of listed company shares. Instead, an issuer, such as Backed Finance or another compliant institution, holds the underlying shares and mints corresponding on-chain tokens at a 1:1 ratio. Users hold digital certificates representing the economic value of the underlying stocks.

The advantages of this model lie in programmability and global transferability. Its risks stem from issuer credit risk, smart contract risk, and regulatory uncertainty that remains unresolved.

Compared with ordinary crypto market trading, tokenized equities are anchored to the fundamentals of real companies, making their price movements relatively more predictable and more closely correlated with macroeconomic cycles. For users holding large amounts of stablecoins, tokenized equities provide a pathway to participate in equity markets without exiting the crypto ecosystem, filling an important product gap.

CFDs, by contrast, are fundamentally price derivatives. Users trade the price movements of an underlying asset rather than the asset itself. Prices are generally quoted by liquidity providers and may be affected by spreads, financing costs, and trading-hour restrictions.

Compared with traditional CFD products, the U.S. stock spot trading services launched by crypto exchanges are structurally much closer to actual securities markets. U.S. stock spot trading generally tracks real equities or corresponding ownership interests directly. The price discovery process is more transparent, allowing prices to more accurately reflect supply and demand while also aligning more closely with the trading habits of traditional investors.

3.1.2 Gate Officially Launches Stock Trading, Bridging the Boundary Between Crypto Assets and Traditional Financial Markets

Gate has officially launched stock trading, allowing users to directly trade stocks, ETFs, and other assets listed on major U.S. securities markets using USDT within the platform.

With the official launch of stock trading services, Gate is further breaking through the boundary between crypto assets and traditional financial markets and accelerating the construction of a unified trading and asset allocation system covering crypto assets, stocks, and mainstream global financial products.

Unlike the tokenized stock and RWA mapping models currently being widely discussed in the market, Gate’s stock service places greater emphasis on market access capability and a compliant trading framework. Through partnerships with compliant brokerage firms, Gate provides stock and ETF trading services rather than on-chain mapped assets or tokenized securities.

In terms of product coverage, while most tokenized stock platforms typically support only several hundred assets, Gate currently supports more than 10,000 stocks and ETF products. These cover assets and liquidity networks from major U.S. securities exchanges, including the NYSE, Nasdaq, NYSE Arca, NYSE American, and BATS. This provides users with broader and more comprehensive opportunities for global securities asset allocation.

At present, Gate Stocks supports regular market-hour trading. In the future, it will gradually expand toward 24/7 trading, providing global users with a more flexible and efficient trading experience.In terms of product structure, Gate Stocks operates independently from traditional CFD systems. Users can buy, hold, and sell stock assets through their Gate accounts, with funds managed separately. Unlike perpetual futures products that involve funding rates, or CFD products that incur swap fees and overnight holding costs, Gate stock spot trading does not involve funding fees or overnight holding charges. This makes it more suitable for users seeking long-term allocation to U.S. equities.

At present, the product supports only market-order buying and selling during regular trading hours. Margin financing and securities lending functions will be introduced gradually in future releases. In addition, Gate plans to support one-click transfers of stock assets between brokerages, further improving asset mobility and cross-platform management efficiency.

Users will also be able to view and manage positions, profit and loss, cash flow records, and corporate actions such as cash dividends, stock splits, and reverse stock splits within a unified account interface. Related proceeds will be automatically credited to user accounts according to platform rules. From an industry perspective, crypto platforms are gradually evolving from single digital asset trading venues into comprehensive trading infrastructure connecting global capital markets.

Gate’s launch of stock trading services not only expands its service boundaries and product capabilities within traditional financial markets, but also signifies its acceleration toward building a unified trading and multi-asset allocation system covering crypto assets, stocks, and a wider range of global financial products. Going forward, Gate will continue advancing market access, global liquidity connectivity, and cross-market trading capabilities, reinforcing its long-term positioning as a global asset trading and market access platform.

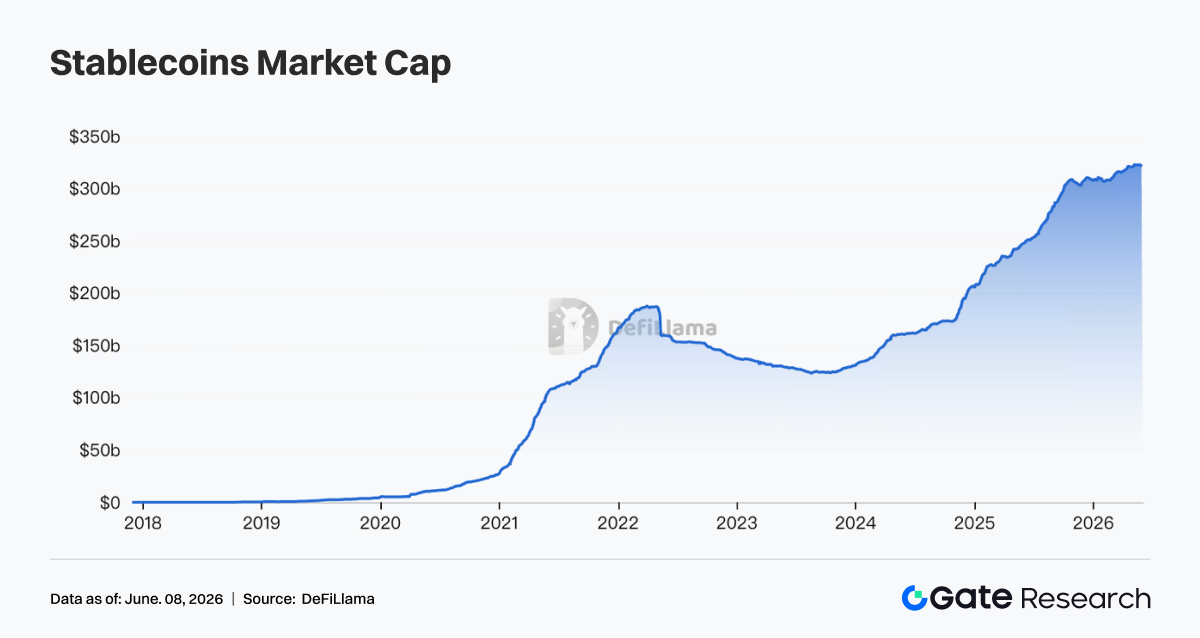

3.2 Stablecoin Market Capitalization Surpasses USD 300 Billion: What Does a Threefold Increase in One Year Mean?

In May 2026, total stablecoin market capitalization officially surpassed USD 300 billion, representing a threefold increase from approximately USD 100 billion one year earlier. This symbolizes a structural transformation across the crypto industry, with stablecoins evolving from a trading medium into a component of global financial infrastructure.

3.2.1 The Growth Logic Behind Stablecoin Market Capitalization

The explosive growth of stablecoins is not driven by a single factor.

First, the establishment of regulatory frameworks has opened the door for institutional capital. From a regulatory perspective, progress on the GENIUS Act has provided stablecoin issuers with a clear compliance pathway. Traditional financial institutions that had previously remained on the sidelines are now able to formally enter the market. These institutions can incorporate stablecoins into corporate balance sheets or use them as channels for cross-border settlement.

This differs fundamentally from the stablecoin growth cycle between 2020 and 2022. During that period, growth was primarily driven by crypto-native trading demand. In the current cycle, growth is supported by genuine business demand from compliant institutions.

Second, demand for dollarization has increased structurally.

Residents in emerging-market countries such as Turkey, Argentina, and Nigeria have long faced depreciation pressures on their local currencies. As a result, the penetration of USDT and USDC in everyday payments continues to increase in these regions. In some areas, stablecoins have already begun replacing local mobile payment applications.

These use cases are largely independent of fluctuations in the crypto market, creating a stable base layer of demand.

Third, the expansion of on-chain finance has significantly increased stablecoin usage.

As RWAs, on-chain lending, and yield-generating products scale up, stablecoins are increasingly being used as settlement layers. The proportion of stablecoins within DeFi TVL continues to rise, meaning that stablecoins are no longer merely “dollars sitting on exchanges.” Instead, they are actively circulating on-chain, generating financial activity and creating value.

3.2.2 Competitive Landscape and Future Regulatory Pathways

It is worth noting that the USD 2.2 billion size of Crypto Fund 5 is smaller than the USD 4.5 billion size of the fourth fund raised in 2022. The market generally believes that this was an intentional reduction by a16z rather than a signal of declining capability. a16z explicitly stated that a shorter fundraising cycle allows them to “keep pace with the evolution of crypto trends.” Behind this lies an important industry judgment: crypto market cycles are becoming shorter and directional shifts are occurring more rapidly, meaning that the deployment cycle of ultra-large funds may instead become a burden. Fund 5 has a clear investment focus: stablecoins, payments, on-chain finance (lending and derivatives), prediction markets, and RWAs. These five sectors share a common characteristic—they are all moving toward real users, real revenue, and real scale, rather than relying on speculative token premiums. a16z explicitly stated that Fund 5 will not invest in AI and will remain 100% focused on crypto, drawing a clear distinction from its AI funds and reflecting a well-defined internal strategic division.

Compared with a16z’s relatively conservative and disciplined approach, Katie Haun’s strategy is more aggressive. She defined the three core investment themes of the new fund as next-generation financial infrastructure, tokenized assets and new markets, and the AI Agent economy. The last theme is particularly noteworthy. As AI Agents increasingly begin performing tasks on behalf of humans, they require autonomous financial capabilities, including payment accounts, credit facilities, identity verification, and fraud prevention. These requirements naturally align with the permissionless and programmable characteristics of blockchain technology. BVNK, one of Haun’s previous investments, was acquired by Mastercard at a valuation of USD 1.8 billion, while Bridge was acquired by Stripe for USD 1.1 billion. Both exits were concentrated in stablecoin infrastructure and validated her investment framework. The new fund extends this logic into the AI Agent economy and is essentially a bet on what kind of financial rails the next generation of internet-native participants will require.

3.3 Crypto VC Funding Rebounds Strongly: The Industry Logic Behind a16z’s USD 2.2 Billion and Haun’s USD 1 Billion Funds

Around May 2026, the crypto venture capital sector experienced a concentrated wave of large-scale fundraising. a16z crypto announced the completion of Crypto Fund 5, its fifth crypto-focused fund, with a total size of USD 2.2 billion. Haun Ventures completed its second fund with USD 1 billion. Dragonfly completed its fourth fund with USD 650 million. Paradigm was reportedly raising a new fund of up to USD 1.5 billion, while Blockchain Capital raised approximately USD 700 million during the same period. Since April, total funding in the crypto sector has reached USD 2.359 billion.

3.3.1 Historical Background of the Fundraising Wave

To understand this fundraising wave, it is first necessary to understand its historical background. The collapse of FTX in 2022 pushed crypto venture capital into a prolonged winter: LPs (limited partners) withdrew capital, fund net asset values declined sharply, and fundraising for new funds nearly came to a standstill. During the recovery period from 2023 to 2024, most VC firms adopted defensive strategies, maintaining operations through relatively small fund sizes. In 2025, Bitcoin reached a new all-time high, and the approval of Bitcoin ETFs in the United States brought nearly USD 60 billion of institutional inflows into the crypto market, effectively resolving the issue of crypto’s legitimacy in the eyes of institutional investors.

By 2026, VCs judged that the timing had become favorable based on three factors. First, as discussed earlier, regulatory frameworks were gradually taking shape through developments such as the GENIUS Act and the Clarity Act, providing a more predictable set of rules. Second, infrastructure from the previous cycle—including Layer 2 networks, cross-chain bridges, and stablecoin payment systems—had matured sufficiently to support an application-layer expansion. Third, the convergence of AI and crypto had begun to demonstrate a clear commercial logic, creating entirely new investment categories.

3.3.2 a16z’s USD 2.2 Billion Fund Is Smaller and More Focused, While Haun’s USD 1 Billion Fund Bets on the AI Agent Economy

It is worth noting that the USD 2.2 billion size of Crypto Fund 5 is smaller than the USD 4.5 billion size of a16z’s fourth crypto fund raised in 2022. The market generally believes that this was an intentional reduction rather than a signal of diminished capability. a16z explicitly stated that a shorter fundraising cycle allows the firm to “keep pace with the evolution of crypto trends.” Behind this statement lies an important industry judgment: crypto market cycles are becoming shorter, and shifts in market direction are occurring more rapidly, meaning that the deployment cycle associated with extremely large funds may become a burden rather than an advantage.

Fund 5 has a clearly defined investment focus: stablecoins, payments, on-chain finance (including lending and derivatives), prediction markets, and RWAs. These five areas share a common characteristic—they are all moving toward real users, real revenue, and real scale rather than relying on speculative token premiums. a16z explicitly stated that Fund 5 will not invest in AI and will remain 100% focused on crypto, drawing a clear distinction from its AI funds and reflecting a clearly defined internal strategic division.

Compared with a16z’s relatively conservative and disciplined approach, Katie Haun’s strategy is more aggressive. She defined the three core investment themes of the new fund as next-generation financial infrastructure, tokenized assets and new markets, and the AI Agent economy. The final theme is particularly noteworthy. As AI Agents increasingly begin performing tasks on behalf of humans, they require autonomous financial capabilities, including payment accounts, credit facilities, identity verification, and fraud prevention. These requirements naturally align with the permissionless and programmable characteristics of blockchain technology.

BVNK, one of Haun’s previous investments, was acquired by Mastercard at a valuation of USD 1.8 billion, while Bridge was acquired by Stripe for USD 1.1 billion. Both exits were concentrated in stablecoin infrastructure and validated her investment framework. The new fund extends this logic into the AI Agent economy and essentially represents a bet on what kind of financial rails the next generation of internet-native participants will require.

3.3.3 Changes in the Structure of Fundraising: Who Is Providing the Capital?

The LP composition behind this fundraising wave differs from that of 2021. In 2021, sovereign wealth funds and university endowments entered the crypto market in large numbers, and some funds even faced the challenge of having more capital than they could effectively deploy. Today, capital is increasingly coming from family offices with deep experience in crypto, strategic corporate investors such as exchanges and market makers, and hedge funds. These LPs generally possess greater tolerance for volatility and a deeper understanding of exit pathways, providing venture capital firms with a more stable capital base.

However, the rebound in venture capital fundraising also introduces a potential concern: there may be too much capital chasing too few projects, causing valuation bubbles to form prematurely. Of the USD 2.359 billion raised since April, capital has been highly concentrated in a small number of leading projects. For early-stage projects, fundraising remains difficult. LPs have become less tolerant of projects built purely on narratives without revenue generation. The market generally views this as a healthy development because capital is becoming more selective, forcing founders to identify product-market fit more quickly rather than relying on token issuance to sustain valuations. Over the long term, this should contribute positively to the overall quality of the industry.

The aggressive fundraising efforts by a16z and Haun represent a collective vote of confidence from institutional capital in the crypto industry’s transition from speculation toward infrastructure. Ultimately, this capital is likely to flow toward areas such as stablecoin payments, RWAs, and financial rails for AI Agents rather than short-term narratives such as NFTs or GameFi. Over the next 18 to 24 months, the pace at which this capital is deployed will directly influence the timeline for the emergence of the next generation of industry-defining projects. For market participants, tracking the investment portfolios of these leading venture capital firms will remain an important reference point for identifying the next major sources of value creation within the industry.

Data Source:

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.