Mega Financial Holding Chairman Dong Rui-bin recently announced the results of a cross-border remittance experiment using stablecoins. The conclusion was that when remittances exceed approximately $7,000 USD, traditional bank transfers have lower overall costs than stablecoins, indicating that conventional finance still holds advantages in clearing and compliance. However, this conclusion has sparked widespread criticism within Taiwan’s crypto community, mainly questioning the experimental design itself. Financial researcher Yu Zhe-an analyzed the potential cognitive blind spots and underlying vested interests behind the design from the perspective of fairness and objectivity.

Details of Mega Financial’s Experimental Design and Core Conclusions

Dong Rui-bin’s experiment involved depositing $50 USDT into an exchange, transferring it via blockchain, then withdrawing on a Taiwanese exchange, and comparing this process with traditional bank cross-border remittance. The results showed that stablecoin transactions incur a fixed fee of about 1 to 2 USDT plus approximately 0.2% transaction fee; bank remittances include a fixed postal fee of NT$300 and a 0.05% transfer fee, totaling between NT$420 and NT$1,100, with a fee cap.

The core conclusion is: for small amounts, stablecoins offer speed and some cost advantages, but when remittance amounts exceed $7,000 USD, bank fees become lower overall, and traditional finance maintains its compliance advantages.

Main Controversy: On-Chain Fee Data and Experimental Conditions

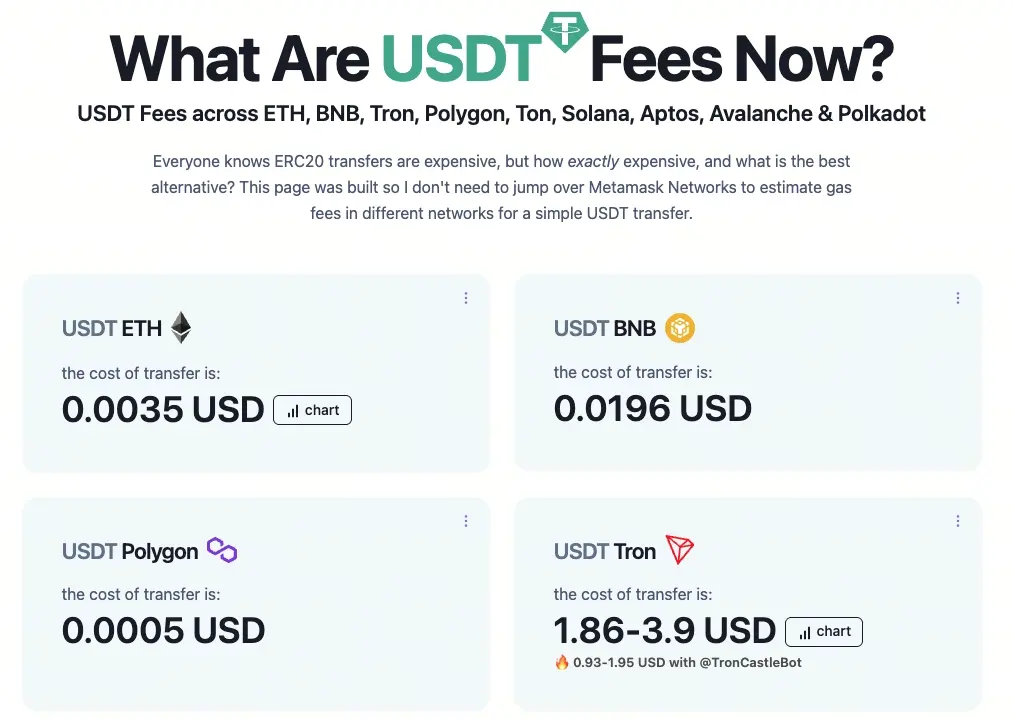

(Source: GasFeesNow)

Ming-en Xu criticized in “Blockchain Power” that the conclusion “banks are more cost-effective than stablecoins above $7,000” is a “Nobel Prize-level innovative statement,” pointing out that USDT transfer fees on blockchain are publicly verifiable and objective data.

He provided actual transfer fee data across different chains, which are significantly lower than the standards set in the experiment:

- Ethereum: $0.0036 USD

- Binance Smart Chain (BSC): $0.0193 USD

- Polygon: $0.0011 USD

- Tron: $1.83 to $3.83 USD (as of afternoon March 11)

Ming-en Xu emphasized that the issue isn’t the cost of stablecoins themselves, but that the experiment included additional costs for “exchange deposit and withdrawal,” making the comparison baseline unequal from the start.

Yu Zhe-an’s Analysis of Design Logic and Potential Interests

Financial researcher Yu Zhe-an offers a deeper analysis. He points out that the focus should not be solely on the conclusion but on what kind of experimental design produced it.

His main argument is: The “objectivity” defined by Dong Rui-bin in this experiment is essentially “regulatory equivalence,” not “technical efficiency.” The experiment fully incorporates exchange deposit and withdrawal costs into the stablecoin’s total cost, which is fair for banks since both parties bear legal jurisdiction and KYC responsibilities. However, for tech companies aiming to improve cross-border payments with stablecoins, deposit and withdrawal through exchanges are unnecessary steps and should not be included in the baseline cost.

His conclusion is thought-provoking: “People only emphasize fairness when they are at a disadvantage, and consumers don’t care whether the competition between banks and stablecoin providers is fair.” In subsequent responses, Yu further inferred that if he worked at a bank and his supervisor asked him to find the weaknesses of stablecoins, “he would naturally design the experiment this way”—implying that institutional biases may have influenced the research framework from the outset.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.