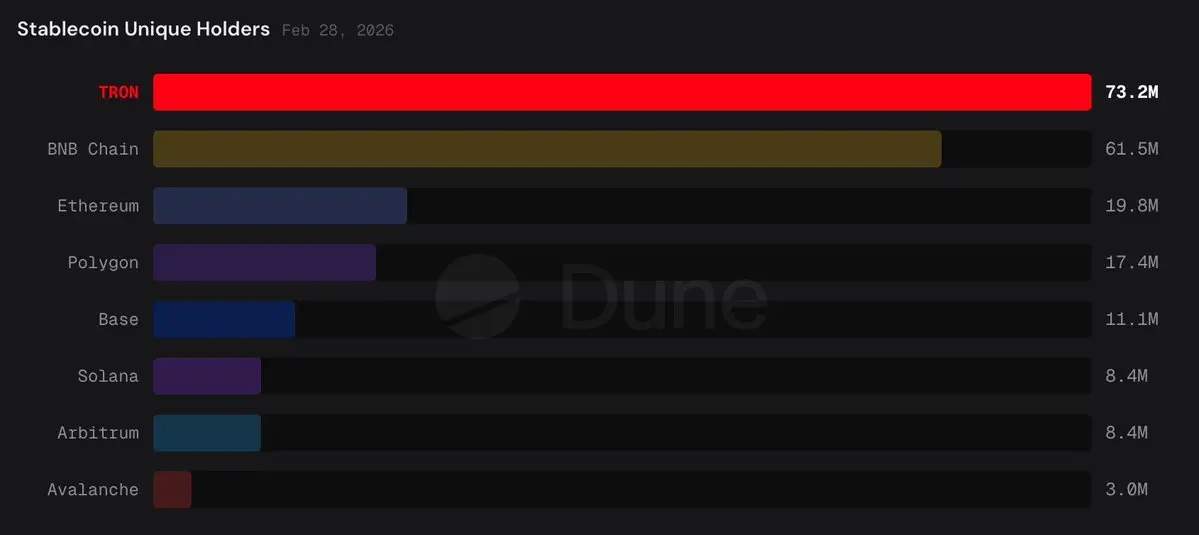

#StablecoinMarketCapHitsANewHigh

The stablecoin market has reached a new peak with an annual growth rate of 50%.

Major institutions like Visa, Mastercard, and JPMorgan have integrated blockchain infrastructure into their systems.

Growth in the market, regulation, and tensions between traditional banks and stablecoin issuers have become prominent.

The total value of the stablecoin market has risen to $312 billion, setting a new record.

This growth marks a statistical milestone as traditional payment giants and large financial institutions adopt blockchain-based systems.

Over the past year, the market value increased by approximately 50%.

During the same period, transfer volume via stablecoins reached $11 trillion.

In addition to Visa and Mastercard, institutions like JPMorgan and Citi have integrated blockchain infrastructure into their payment and transfer services.

The total volume of dollar-based transfers on blockchain reached $11 trillion last year.

While Visa is known for processing about $12 trillion annually, the stablecoin market volume is approaching this size.

A financial asset class that did not exist just 15 years ago is now approaching the same level as today’s leading card payment infrastructure, drawing attention in the financial ecosystem.

The 50% annual growth rate in the stablecoin market highlights its potential for future development.

If the market value continues to grow at this pace, the new target level could reach $468 billion within a year.

Current data indicates that the growth rate is not slowing down.

Visa and Mastercard have already begun on-chain payments and transaction processes using USDC.

This eliminates the previously required correspondent bank infrastructure for card payments.

JPMorgan, Citi, and HSBC are conducting pilot programs related to tokenized deposits and blockchain-based payment services.

Additionally, Mastercard has partnered with SoFi Technologies to enable real-time inter-company money transfers and cross-border payments using SoFiUSD.

These developments are not limited to crypto-focused companies; major players in the international financial markets are also starting to incorporate stablecoin technology into their products for millions of customers.

What began as a speculative trading tool has now become a fundamental component of the financial infrastructure.

Aon, a company operating in financial services, has launched a pilot program to facilitate the payment of insurance premiums with stablecoins.

Circle Payments Network stands out as a service supporting international money transfers in regions such as the US, EU, Singapore, India, and the Philippines.

These developments indicate that stablecoin infrastructure is integrating into the global financial system faster than expected.

Market Share and Regulatory Agenda

Tether holds approximately 59% of the market with USDT.

Circle’s USDC accounts for about 25%.

Together, these two assets control 84% of the market.

Among new entrants, Sky’s USDS has reached a market value of $7.9 billion, becoming one of the rapidly growing products.

This growth also reflects in regulatory discussions.

In particular, the GENIUS Act in the US and the MiCA regulation in Europe are establishing clear operational rules for stablecoin issuers.

Similar regulations are being prepared in the Asia-Pacific region.

In the US, the legal foundation for Aon’s pilot program is based on the GENIUS Act.

In Europe, MiCA provides a clear framework for regulated issuers.

There is a noticeable trend of significant institutional adoption worldwide.

Conflict of Interest Between Banks and Stablecoin Issuers

The $312 billion value of the stablecoin market indicates that this amount is moving outside the traditional banking sector.

While JPMorgan is testing tokenized deposits as a pilot, it is also lobbying against regulations that would require paying interest on deposits.

Similarly, banks that have integrated stablecoin infrastructure into their products are pursuing legal action claiming stablecoin issuers should not need a banking license.

This opposition points to ongoing tension between the need to enhance financial infrastructure efficiency and the revenue models provided by the current system.

Traditional institutions are trying to protect their interests while adapting to new technologies.

The stablecoin market has reached a new peak with an annual growth rate of 50%.

Major institutions like Visa, Mastercard, and JPMorgan have integrated blockchain infrastructure into their systems.

Growth in the market, regulation, and tensions between traditional banks and stablecoin issuers have become prominent.

The total value of the stablecoin market has risen to $312 billion, setting a new record.

This growth marks a statistical milestone as traditional payment giants and large financial institutions adopt blockchain-based systems.

Over the past year, the market value increased by approximately 50%.

During the same period, transfer volume via stablecoins reached $11 trillion.

In addition to Visa and Mastercard, institutions like JPMorgan and Citi have integrated blockchain infrastructure into their payment and transfer services.

The total volume of dollar-based transfers on blockchain reached $11 trillion last year.

While Visa is known for processing about $12 trillion annually, the stablecoin market volume is approaching this size.

A financial asset class that did not exist just 15 years ago is now approaching the same level as today’s leading card payment infrastructure, drawing attention in the financial ecosystem.

The 50% annual growth rate in the stablecoin market highlights its potential for future development.

If the market value continues to grow at this pace, the new target level could reach $468 billion within a year.

Current data indicates that the growth rate is not slowing down.

Visa and Mastercard have already begun on-chain payments and transaction processes using USDC.

This eliminates the previously required correspondent bank infrastructure for card payments.

JPMorgan, Citi, and HSBC are conducting pilot programs related to tokenized deposits and blockchain-based payment services.

Additionally, Mastercard has partnered with SoFi Technologies to enable real-time inter-company money transfers and cross-border payments using SoFiUSD.

These developments are not limited to crypto-focused companies; major players in the international financial markets are also starting to incorporate stablecoin technology into their products for millions of customers.

What began as a speculative trading tool has now become a fundamental component of the financial infrastructure.

Aon, a company operating in financial services, has launched a pilot program to facilitate the payment of insurance premiums with stablecoins.

Circle Payments Network stands out as a service supporting international money transfers in regions such as the US, EU, Singapore, India, and the Philippines.

These developments indicate that stablecoin infrastructure is integrating into the global financial system faster than expected.

Market Share and Regulatory Agenda

Tether holds approximately 59% of the market with USDT.

Circle’s USDC accounts for about 25%.

Together, these two assets control 84% of the market.

Among new entrants, Sky’s USDS has reached a market value of $7.9 billion, becoming one of the rapidly growing products.

This growth also reflects in regulatory discussions.

In particular, the GENIUS Act in the US and the MiCA regulation in Europe are establishing clear operational rules for stablecoin issuers.

Similar regulations are being prepared in the Asia-Pacific region.

In the US, the legal foundation for Aon’s pilot program is based on the GENIUS Act.

In Europe, MiCA provides a clear framework for regulated issuers.

There is a noticeable trend of significant institutional adoption worldwide.

Conflict of Interest Between Banks and Stablecoin Issuers

The $312 billion value of the stablecoin market indicates that this amount is moving outside the traditional banking sector.

While JPMorgan is testing tokenized deposits as a pilot, it is also lobbying against regulations that would require paying interest on deposits.

Similarly, banks that have integrated stablecoin infrastructure into their products are pursuing legal action claiming stablecoin issuers should not need a banking license.

This opposition points to ongoing tension between the need to enhance financial infrastructure efficiency and the revenue models provided by the current system.

Traditional institutions are trying to protect their interests while adapting to new technologies.