With the rapid growth of stablecoins, digital assets, and on-chain payments, market demand for bank-grade blockchain infrastructure is accelerating. Traditional banking systems offer mature payment and account management capabilities, but face limitations in digital asset access, cross-border settlement efficiency, and global openness. Meanwhile, most DeFi protocols focus mainly on lending, trading, or liquidity management, making it difficult to deliver a full banking service experience.

WeFi introduces the Deobank (decentralized banking) model against this backdrop. Rather than a single financial protocol, WeFi prioritizes the integrated operation of account systems, payment networks, asset management, and financial services.

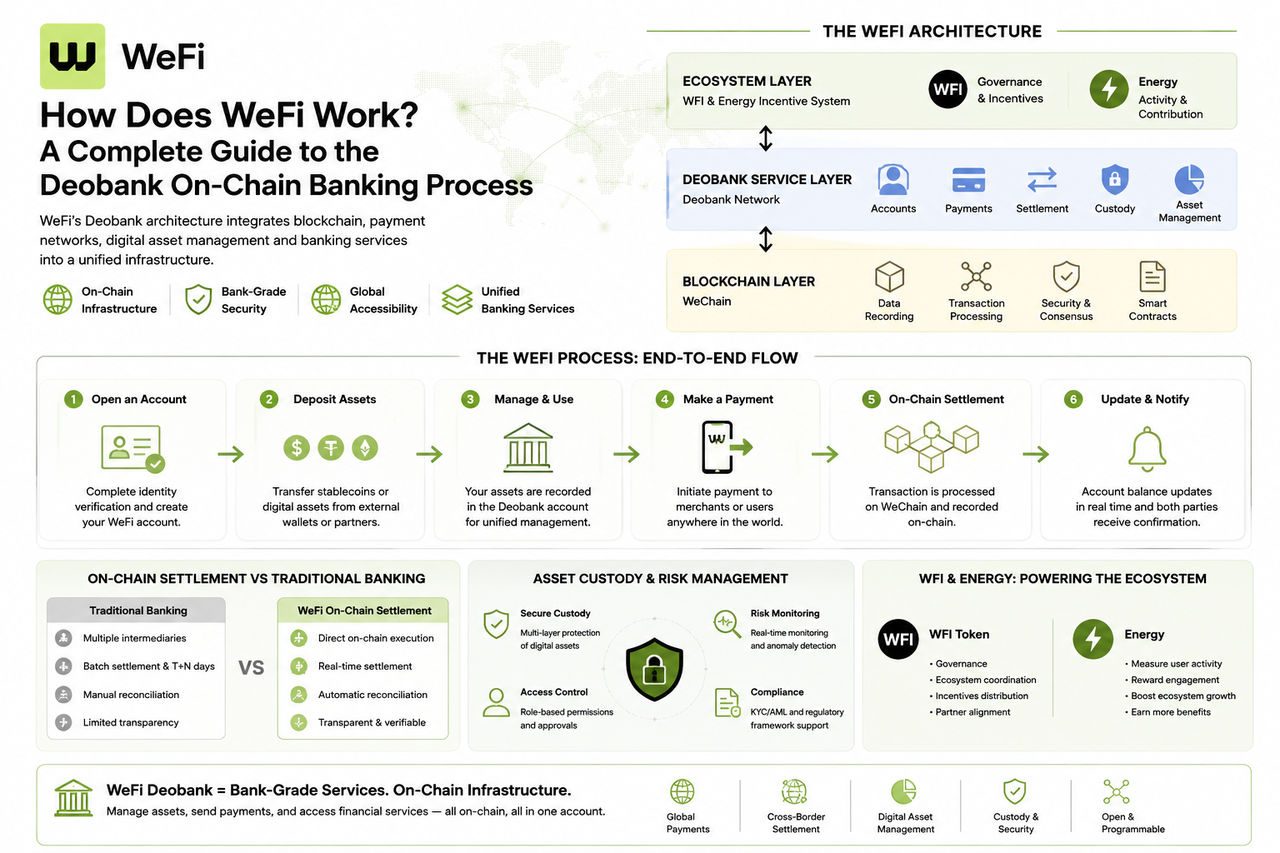

WeFi Operational Framework at a Glance

WeFi's operational logic can be viewed as a multi-layered financial services network.

The bottom layer, WeChain, handles data recording and transaction settlement. The middle layer, the Deobank Network, delivers account, payment, and asset management services. The top layer uses the WFI and Energy incentive systems to coordinate the relationships among users, partners, and ecosystem participants.

The system's overarching goal is to let users manage assets as intuitively as they would with a traditional bank, while retaining the transparency and openness of a blockchain network.

| Architecture Layer |

Core Components |

Primary Responsibilities |

| Incentive and Governance Layer |

WFI, Energy |

Governance and ecosystem incentives |

| Service Layer |

Deobank Network |

Banking services and payment network |

| Infrastructure Layer |

WeChain |

Data recording and on-chain settlement |

What Is Deobank?

Deobank is the foundational concept of the WeFi ecosystem, describing a blockchain-based banking service system.

Traditional banks rely on centralized institutions to manage accounts and funds. Deobank, by contrast, emphasizes on-chain records, open access, and digital asset compatibility. Users gain account management, payment settlement, and asset services while benefiting from the transparency of the blockchain network.

Functionally, Deobank is best understood as "banking service infrastructure" rather than a single financial protocol or payment tool.

What Happens After a User Opens an Account?

The first step for users entering the WeFi network is typically account creation.

Unlike traditional wallets that only manage on-chain addresses, WeFi's account design mirrors the bank account concept. The account serves as a unified portal for managing digital assets, payment permissions, and financial services.

After completing identity verification and account setup, users can tap into the WeFi service network, gaining payment, custody, and asset management capabilities.

Account creation is the starting point of the entire Deobank service journey and the critical link connecting users to the ecosystem.

How Do Digital Assets Enter the WeFi Ecosystem?

Once the account is established, users need to bring their digital assets onto the network.

Assets can originate from external wallets, stablecoin accounts, or partner-provided channels. Once inside the WeFi network, assets are recorded in the unified account system and synchronized via the on-chain network.

This process enables assets to participate in payments, settlements, custody, and other financial services.

From a system perspective, asset onboarding effectively connects user funds to the Deobank network.

How Does the WeFi Payment Process Work?

Payment is one of WeFi's most vital use cases.

When a user initiates a payment request, the system first validates account permissions and asset balance, then submits the transaction details to the underlying network for processing.

Once the transaction enters WeChain, it is confirmed and recorded. The payment result is synced to the relevant account, and the asset status is updated.

The process parallels a traditional bank payment flow, but settlement records can be verified on the blockchain, boosting transparency and traceability.

| Payment Stage |

System Action |

| Payment Initiation |

User submits transaction request |

| Verification Stage |

Check account permissions and balance |

| Network Processing |

WeChain executes the transaction |

| Settlement Confirmation |

Update account status |

| Result Synchronization |

Complete payment record |

How Is On-Chain Settlement Different from Traditional Bank Settlement?

Traditional bank settlement relies on data synchronization and fund clearing across multiple financial institutions.

WeFi's on-chain settlement records transaction results directly on the blockchain. Once a transaction is confirmed, all parties can verify the status using the unified ledger.

This approach eliminates redundant reconciliation processes and improves the efficiency of cross-border payments and digital asset transfers.

For use cases requiring real-time fund movement, on-chain settlement delivers a higher degree of automation.

How Are Asset Custody and Risk Management Implemented?

Digital asset management is a key component of the Deobank system.

WeFi's design prioritizes digital asset security, access control, and compliance management. User asset management typically combines account permissions, on-chain records, and risk control mechanisms.

In financial service scenarios, the custody system handles not only asset preservation but also payment authorization, risk identification, and fund flow monitoring.

Thus, the custody system serves as critical infrastructure linking the account system and financial services.

The Role of WFI and Energy in the Operational Process

Beyond payments and account systems, ecosystem incentives are central to WeFi's operation.

WFI, the ecosystem's native token, handles governance, ecosystem coordination, and certain incentive functions. Users, partners, and network participants can engage in ecosystem governance through WFI.

Energy functions as an activity and contribution metric. When users make payments, hold assets, or participate in ecosystem activities, they earn Energy rewards.

This dual-layer mechanism simultaneously addresses long-term governance needs and daily user growth targets.

| Dimension |

WFI |

Energy |

| Positioning |

Native token |

Incentive system |

| Function |

Governance and ecosystem coordination |

User growth and rewards |

| Acquisition Method |

Ecosystem participation |

Service usage behavior |

| Main Objective |

Long-term value coordination |

User activity growth |

What Are the Differences between WeFi and Traditional Banking Processes?

From a user experience standpoint, both WeFi and traditional banks offer account management, payment, and asset services.

However, the underlying architectures differ significantly.

Traditional banks rely on centralized databases, institutional audits, and internal clearing systems. WeFi leverages blockchain networks for data recording and value settlement, allowing digital assets to participate directly in financial activities.

Furthermore, WeFi emphasizes global openness and digital asset compatibility, while traditional banks primarily serve fiat currency systems.

These differences drive distinct operating models, settlement logic, and service scope.

Conclusion

WeFi's operational model is built on the Deobank concept, coordinating core components like WeChain, the Deobank Network, WFI, and Energy. The full process spans account creation, asset onboarding, payment execution, on-chain settlement, asset custody, and ecosystem incentives.

Compared to the traditional banking system, WeFi migrates certain financial service functions to the blockchain network, connecting payments, digital assets, and financial services through a unified account system. Its core aim is not to replace banks, but to build a more open and programmable financial infrastructure for the digital asset era.

FAQs

What is the core of how WeFi operates?

WeFi's core is the Deobank architecture, which uses a blockchain network to integrate account systems, payment services, asset management, and financial infrastructure. This enables digital assets to be managed and used like funds in a bank account.

How is WeFi different from a regular crypto wallet?

Regular crypto wallets primarily manage on-chain assets and addresses. WeFi goes further by emphasizing account systems, payment networks, and financial service capabilities, making its functional scope more akin to a digital banking platform.

How are WeFi payment transactions completed?

After a user initiates a payment, the system verifies account information and asset balance. The transaction is confirmed and settled via WeChain, and the account status is updated accordingly.

Why does WeFi need the WFI token?

WFI is used for ecosystem governance, incentive distribution, and network coordination. It is a key tool connecting users, partners, and protocol governance.

What role does Energy play in WeFi?

Energy is a vital part of the ecosystem incentive system, measuring user activity and ecosystem contribution. It also participates in certain reward distribution mechanisms.