Trade

Trading Type

Spot

Trade crypto freely

Pre-Market

Trade new tokens before they are officially listed

Margin

Magnify your profit with leverage

Convert & Block Trading

0 Fees

Trade any size with no fees and no slippage

Alpha

Points

Get promising tokens in streamlined on-chain trading

Leveraged Tokens

Get exposure to leveraged positions simply

Futures

Futures

Hundreds of contracts settled in USDT or BTC

Options

HOT

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

NEW

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

NEW

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

NEW

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

Promotions

Activity Center

Join activities and win big cash prizes and exclusive merch

Referral

20 USDT

Earn 40% commission or up to 500 USDT rewards

Announcements

Announcements of new listings, activities, upgrades, etc

Gate Blog

Crypto industry articles

VIP Services

Huge fee discounts

Proof of Reserves

Gate promises 100% proof of reserves

Metaplanet 2025 achieves a perfect conclusion! Invested $448 million to increase Bitcoin holdings, surpassing 35,000 coins in total holdings.

42m ago

Year-end final sprint? Strategy spends 108 million to buy again, with a total Bitcoin holding of 672,497 coins

2h ago

Trending Topics

View More2.41K Popularity

152.24K Popularity

23.74K Popularity

75.94K Popularity

1.72K Popularity

Hot Gate Fun

View More- MC:$3.56KHolders:10.00%

- MC:$3.56KHolders:10.00%

- MC:$3.55KHolders:10.00%

- MC:$3.54KHolders:10.00%

- MC:$3.54KHolders:10.00%

Pin

New Version, Worth Being Seen! #GateAPPRefreshExperience

🎁 Gate APP has been updated to the latest version v8.0.5. Share your authentic experience on Gate Square for a chance to win Gate-exclusive Christmas gift boxes and position experience vouchers.

How to Participate:

1. Download and update the Gate APP to version v8.0.5

2. Publish a post on Gate Square and include the hashtag: #GateAPPRefreshExperience

3. Share your real experience with the new version, such as:

Key new features and optimizations

App smoothness and UI/UX changes

Improvements in trading or market data experience

Your fa🎉 Share Your 2025 Year-End Summary & Win $10,000 Sharing Rewards!

Reflect on your year with Gate and share your report on Square for a chance to win $10,000!

👇 How to Join:

1️⃣ Click to check your Year-End Summary: https://www.gate.com/competition/your-year-in-review-2025

2️⃣ After viewing, share it on social media or Gate Square using the "Share" button

3️⃣ Invite friends to like, comment, and share. More interactions, higher chances of winning!

🎁 Generous Prizes:

1️⃣ Daily Lucky Winner: 1 winner per day gets $30 GT, a branded hoodie, and a Gate × Red Bull tumbler

2️⃣ Lucky Share Draw: 10🎨 Gate AI Creation Contest | One Sentence, Draw Your 2026

On Gate Square, anyone can be a visual creator — truly zero barriers to entry.

With just one sentence, generate an image and bring your vision of 2026 to life.

Create and post your work using Gate Square AI Creation for a chance to win the Gate Year of the Horse New Year Gift Box.

📅 Duration

Dec 17, 2025, 10:00 – Jan 3, 2026, 18:00 UTC

🎯 How to Join

1. Go to Gate Square → Create Post → AI Creation

2. Enter one sentence to generate your image

3. Post with #GateAICreation

🏆 Rewards

5 winners: Gate Year of the Horse New Year

PANews 2025 Annual Public Chain Data Review: "Naked Swimming" Moment, Who Is Growing Against the Trend?

Author: Frank, PANews

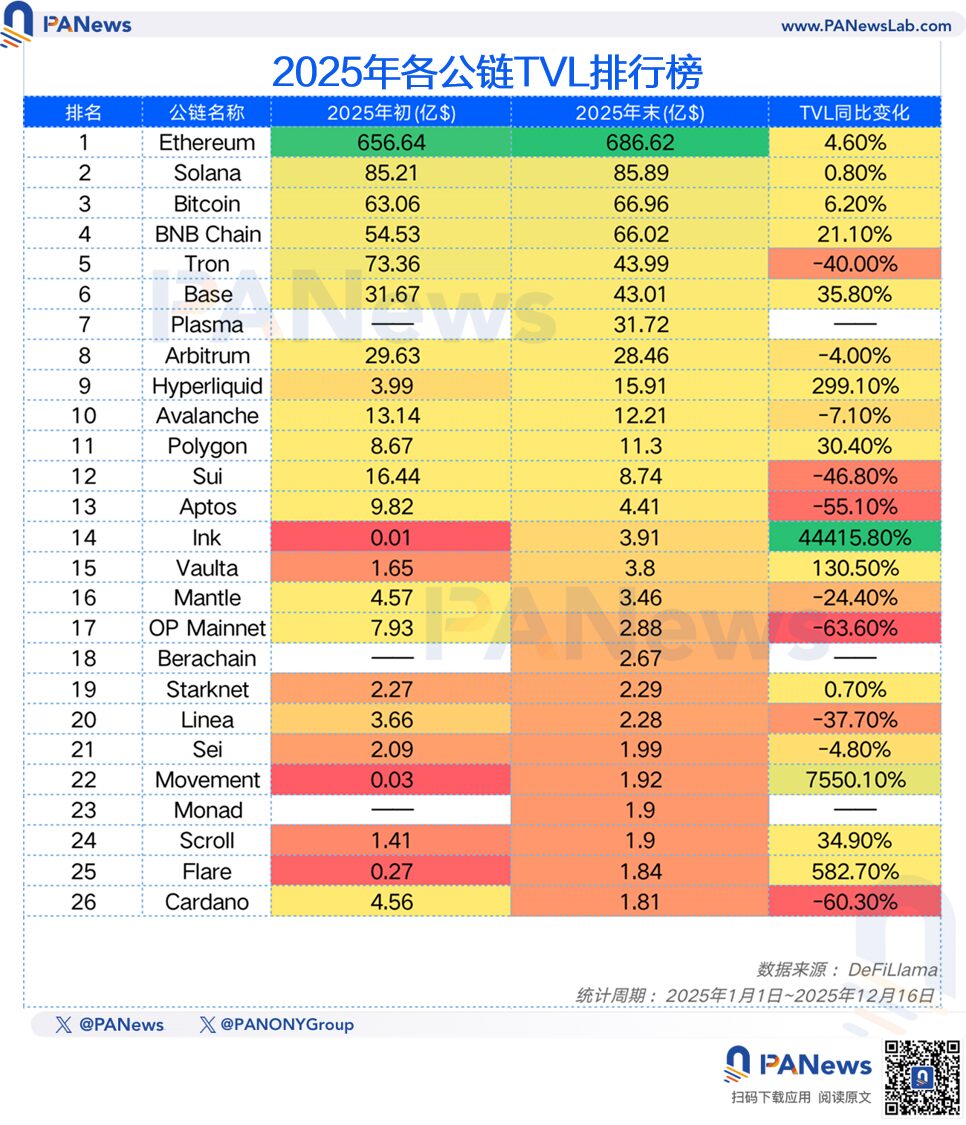

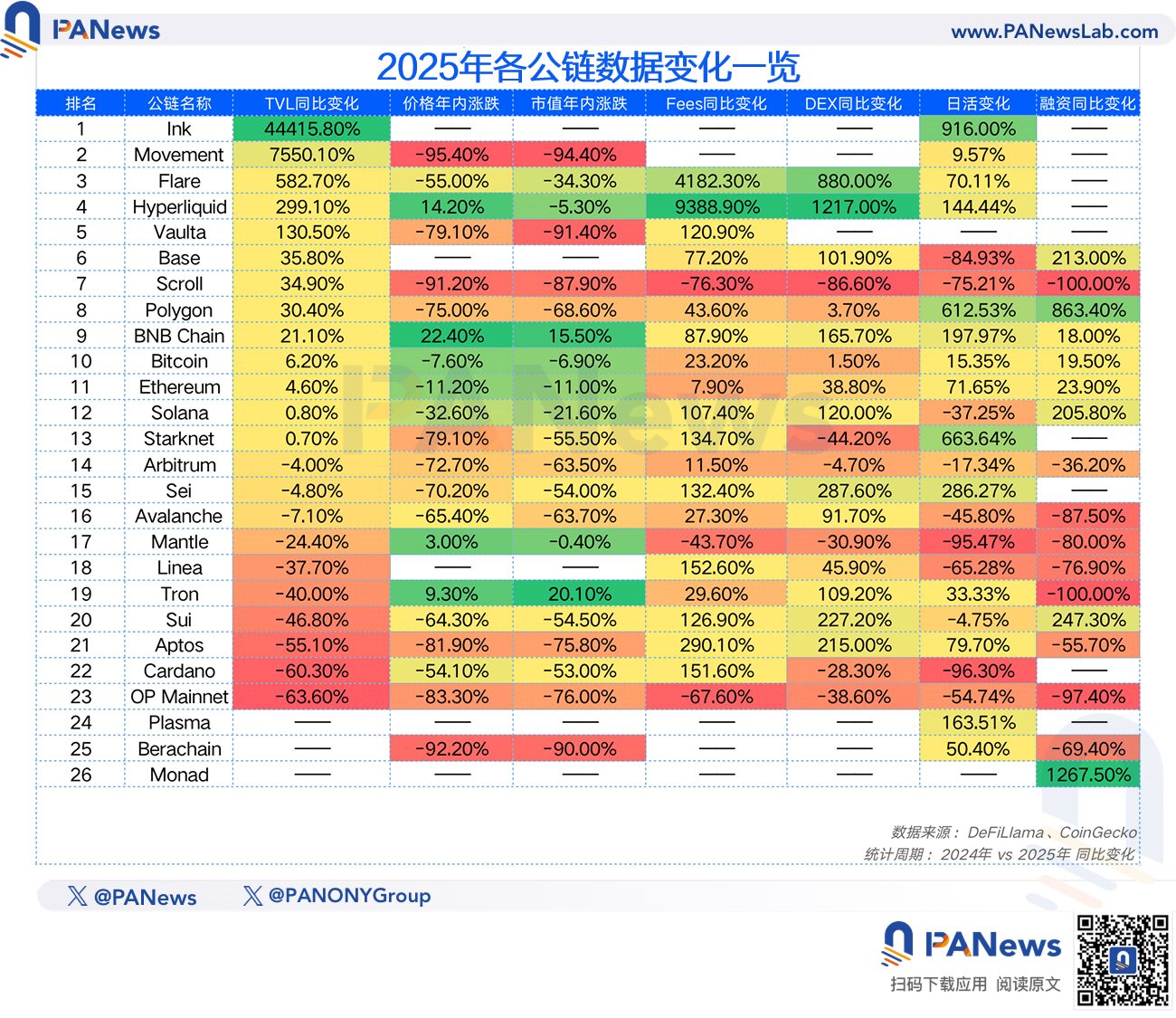

2025 is a year of great drama and a watershed for the public chain track in the crypto world. If 2024 was a “carnival night” where various new public chains competed fiercely with high airdrop expectations and grand narratives, then 2025 is the “wake-up call” after the carnival. As the tide recedes and liquidity tightens, the true data hidden behind the surface of prosperity begins to surface. We see a “clash of two worlds”: on one side, the widespread halving of secondary market prices and a significant slowdown in TVL growth; on the other, an逆 surge in on-chain fee income and DEX trading volume. This stark contrast reveals a cruel truth: the market no longer buys into simple “narratives,” and capital is concentrating on leading protocols with血液造血能力 and essential use cases. PANews’ data team has comprehensively compiled core data from 26 mainstream public chains in 2025. From TVL, token prices, fee income, activity levels to investment and financing, we attempt to restore the “bubble squeezing” process experienced by the public chain market this year through these cold numbers, and to find those true winners who can still build solid moats in the winter. (Data notes: TVL, stablecoins, financing, and fee data are from Defillama; daily active users and daily transaction volume data are from Artemis and on-chain info; token prices and market caps are from Coingecko. The data period is from January 1 to December 16, 2025.) The state of TVL: a cliff-like slowdown in growth, DeFi experiencing “deleveraging” pain Looking at the most important indicator of public chain prosperity, TVL, this year’s top public chains saw slight growth overall but with a slowdown. PANews’ statistics show that the total TVL of 26 major public chains grew by 5.89% this year, with 5 new chains entering the list with initial data of zero. Additionally, only 11 chains achieved positive growth, accounting for about 42%. In comparison, in 2024, the 22 mainstream chains’ annual TVL growth was 119%, with a growth rate of 78%. The slowdown in TVL growth also reflects the overall coldness of the crypto market. But this does not mean 2025 was completely dull. Looking at the entire industry, the network’s TVL reached $168 billion in October, a 45% increase from $115.7 billion at the start of the year. However, after October, due to market crashes, the overall TVL shrank sharply. Part of this was due to the decline in the prices of base tokens of various chains, and part was due to market risk aversion leading many funds to withdraw from DeFi systems. Among the top ten chains, Hyperliquid is clearly the winner of 2025, with a 299% increase in TVL this year, compared to single-digit growth of other chains. Solana, on the other hand, is the most disappointing, with only 0.8% growth. As the MEME coin market cooled, this giant chain seems to be facing a crisis. Additionally, among the 26 chains, Flare’s growth rate exceeded 582%, making it the fastest-growing chain. OP Mainnet’s TVL fell by 63.6%, making it the most severely declining chain. Average token prices halved by 50%, the market no longer supports new chains

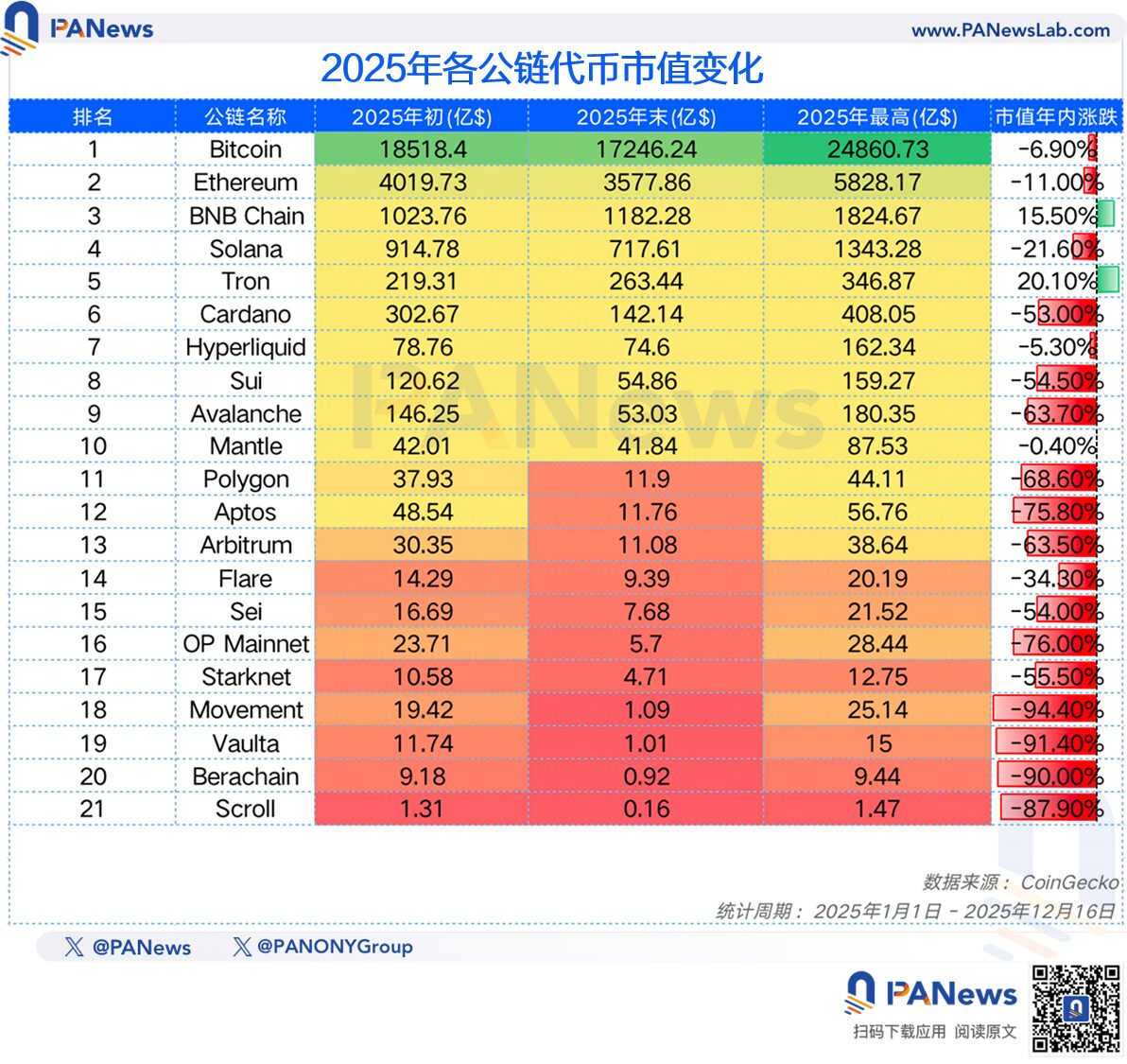

In terms of prices, the performance of these mainstream chains this year was also underwhelming. Compared to their prices at the start of the year, the tokens of these 26 chains fell by an average of 50%. Among them, Movement tokens dropped 95%, Berachain tokens fell 92%, and Scroll declined 91%. These new chains have not gained market recognition.

Among the chains tracked, only BNB Chain (22%), Hyperliquid (14.2%), Tron (9.3%), and Mantle (3%) saw price increases this year; the rest experienced declines.

Average token prices halved by 50%, the market no longer supports new chains

In terms of prices, the performance of these mainstream chains this year was also underwhelming. Compared to their prices at the start of the year, the tokens of these 26 chains fell by an average of 50%. Among them, Movement tokens dropped 95%, Berachain tokens fell 92%, and Scroll declined 91%. These new chains have not gained market recognition.

Among the chains tracked, only BNB Chain (22%), Hyperliquid (14.2%), Tron (9.3%), and Mantle (3%) saw price increases this year; the rest experienced declines.

However, the changes behind TVL and price data are mainly influenced by liquidity shifts in the crypto market. Analyzing the development indicators of the public chain ecosystem reveals a different picture.

Protocol revenue surges, public chains move into a new “self-sustaining” phase

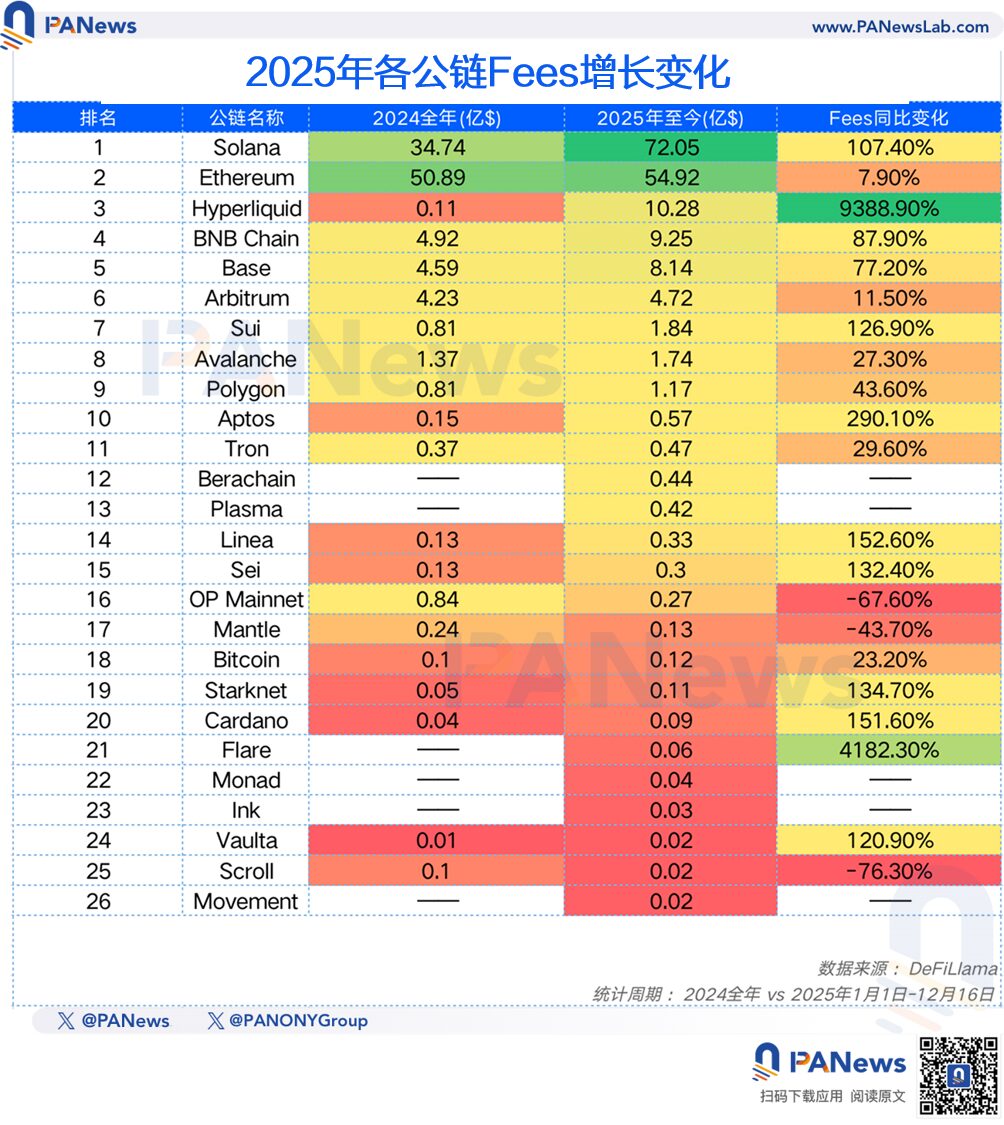

In terms of on-chain fee generation, these chains collectively generated $10.4 billion in fees in 2024, which increased to $16.75 billion in 2025, a total growth of 60%. Moreover, except for OP Mainnet, Mantle, and Scroll, which saw declines in fees, all other chains achieved growth in 2025.

The largest increase in fees was seen in Hyperliquid (9388.9%), mainly because Hyperliquid launched at the end of 2024 with a small initial base. Additionally, Solana’s fees grew by 107%, BNB Chain by 77%, Sui by 126%, and Aptos by 290%. It can be said that the revenue-generating capacity of mainstream public chains greatly improved in 2025.

However, the changes behind TVL and price data are mainly influenced by liquidity shifts in the crypto market. Analyzing the development indicators of the public chain ecosystem reveals a different picture.

Protocol revenue surges, public chains move into a new “self-sustaining” phase

In terms of on-chain fee generation, these chains collectively generated $10.4 billion in fees in 2024, which increased to $16.75 billion in 2025, a total growth of 60%. Moreover, except for OP Mainnet, Mantle, and Scroll, which saw declines in fees, all other chains achieved growth in 2025.

The largest increase in fees was seen in Hyperliquid (9388.9%), mainly because Hyperliquid launched at the end of 2024 with a small initial base. Additionally, Solana’s fees grew by 107%, BNB Chain by 77%, Sui by 126%, and Aptos by 290%. It can be said that the revenue-generating capacity of mainstream public chains greatly improved in 2025.

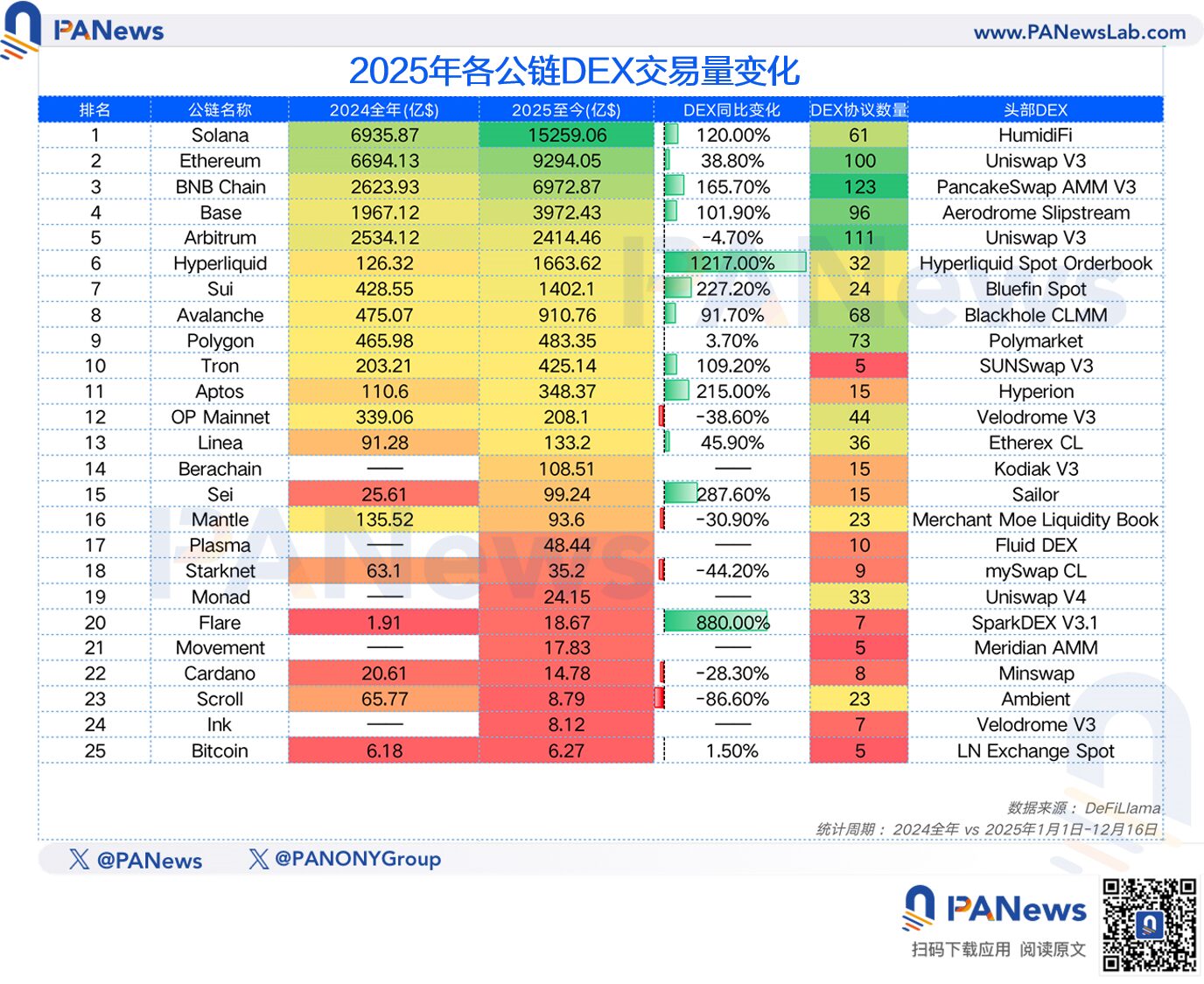

Furthermore, the trading volume on DEXs across chains also grew by 88% overall, with an average increase of 163%. Notably, Solana surpassed Ethereum with a trading volume of $1.52 trillion, ranking the highest, while BNB Chain followed closely with $697.2 billion, making it very likely to overtake Ethereum in 2026.

Hyperliquid remains the fastest-growing, with a 1217.00% increase in DEX trading volume for the year, and Flare ranks second with an 880% increase.

Furthermore, the trading volume on DEXs across chains also grew by 88% overall, with an average increase of 163%. Notably, Solana surpassed Ethereum with a trading volume of $1.52 trillion, ranking the highest, while BNB Chain followed closely with $697.2 billion, making it very likely to overtake Ethereum in 2026.

Hyperliquid remains the fastest-growing, with a 1217.00% increase in DEX trading volume for the year, and Flare ranks second with an 880% increase.

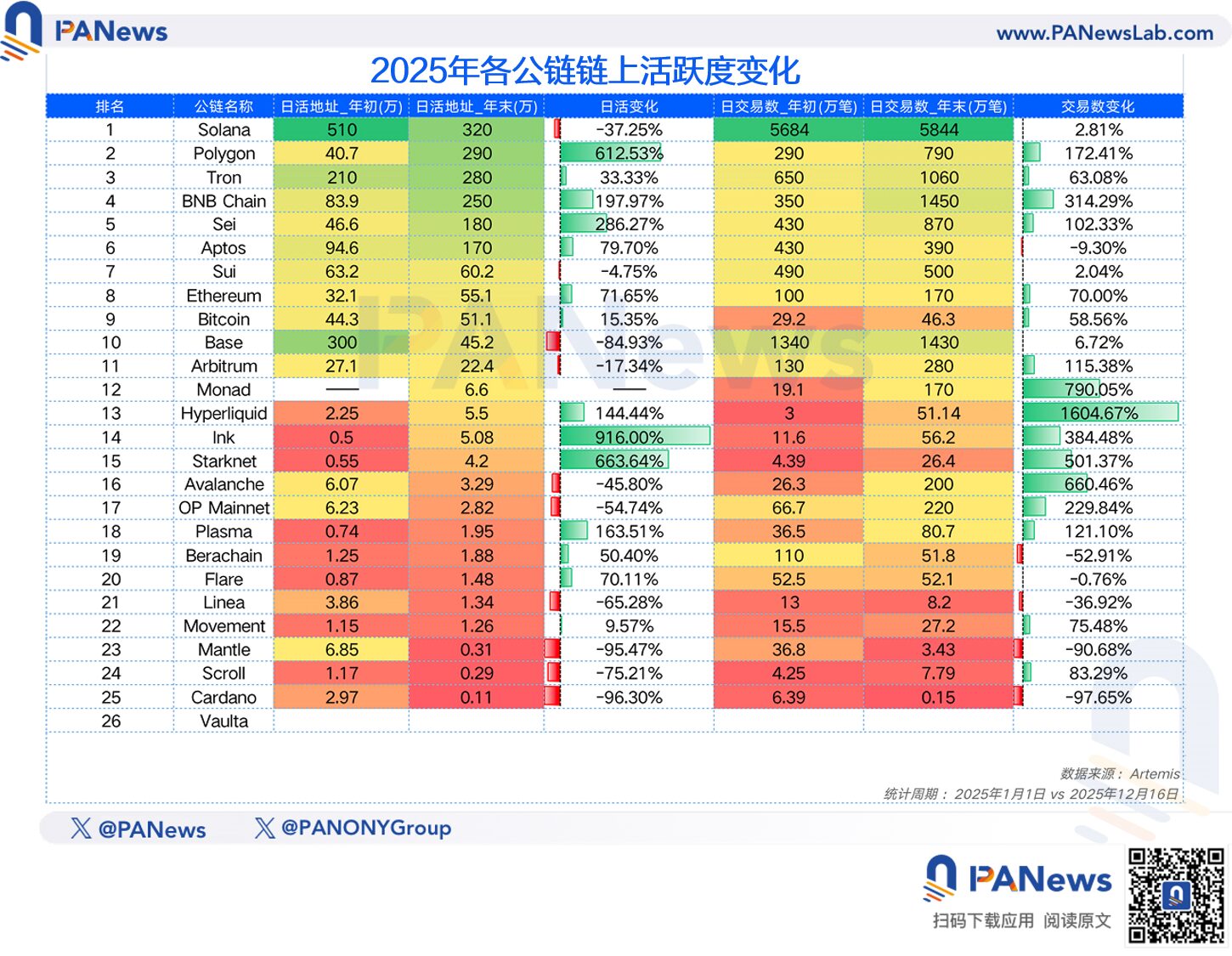

When “airdrop hunters” disperse, retaining new public chain users becomes difficult

In terms of daily active users, the data shows mixed feelings.

Overall, the number of daily active addresses across these chains increased from 14.86 million to 17.6 million, an 18% increase. Achieving such a result in a sluggish market is a relatively positive signal.

However, on the other hand, chains like Solana, Base, and Sui—once considered the most active among retail users—showed varying degrees of decline, with Base’s daily active users dropping 84.9% from the start of the year, and Solana down 37%. Recently, Polygon’s daily active addresses experienced exponential growth, reaching 2.9 million on December 19, a 612% increase from the start of the year. Additionally, chains like BNB Chain, Sei, and Aptos also saw significant growth in daily active users.

Moreover, in terms of daily transaction counts, these chains overall increased by 33% from the beginning of the year. BNB Chain’s data was particularly impressive, growing from 3.5 million to 14.5 million transactions, demonstrating strong scale and growth. Solana still leads with 58.44 million transactions, but with only 2.8% growth for the year, showing signs of fatigue.

When “airdrop hunters” disperse, retaining new public chain users becomes difficult

In terms of daily active users, the data shows mixed feelings.

Overall, the number of daily active addresses across these chains increased from 14.86 million to 17.6 million, an 18% increase. Achieving such a result in a sluggish market is a relatively positive signal.

However, on the other hand, chains like Solana, Base, and Sui—once considered the most active among retail users—showed varying degrees of decline, with Base’s daily active users dropping 84.9% from the start of the year, and Solana down 37%. Recently, Polygon’s daily active addresses experienced exponential growth, reaching 2.9 million on December 19, a 612% increase from the start of the year. Additionally, chains like BNB Chain, Sei, and Aptos also saw significant growth in daily active users.

Moreover, in terms of daily transaction counts, these chains overall increased by 33% from the beginning of the year. BNB Chain’s data was particularly impressive, growing from 3.5 million to 14.5 million transactions, demonstrating strong scale and growth. Solana still leads with 58.44 million transactions, but with only 2.8% growth for the year, showing signs of fatigue.

Stablecoins become the only “bull market” in 2025

The stablecoin market in 2025 experienced a full-blown explosion, which is also reflected in public chain data. Compared to 2024, most chains saw significant increases in stablecoin market cap, with Solana leading with a 196% surge, making it the chain with the largest stablecoin growth. Ethereum and Tron, as the top two chains for stablecoins, maintained annual growth of 46% and 37%, respectively. Additionally, some active chains this year, like BNB Chain and Hyperliquid, also achieved substantial growth in stablecoins.

Stablecoins become the only “bull market” in 2025

The stablecoin market in 2025 experienced a full-blown explosion, which is also reflected in public chain data. Compared to 2024, most chains saw significant increases in stablecoin market cap, with Solana leading with a 196% surge, making it the chain with the largest stablecoin growth. Ethereum and Tron, as the top two chains for stablecoins, maintained annual growth of 46% and 37%, respectively. Additionally, some active chains this year, like BNB Chain and Hyperliquid, also achieved substantial growth in stablecoins.

Ecosystem Financing: Polygon wins with star projects, Ethereum and Solana remain hot

Another data point worth noting is financing activity. In 2025, the crypto industry set a new record with 6,710 financing events, categorized by chain. The data shows that the number of financing deals dropped sharply from 640 to 293, but the total amount increased from $350 million to $667 million, with the average deal size rising from $5.57 million to $22.79 million. This indicates that, currently, it is more difficult for small and medium startups to secure funding, while capital is more willing to invest heavily in star projects.

In terms of chain categories, Polygon raised the most with $2.24 billion, followed by Ethereum with $1.57 billion and Solana with $1.34 billion. However, Polygon’s leading position is mainly due to Polymarket’s massive $2 billion+ funding. Looking at the number of financing events, most occurred within the Ethereum, Solana, Bitcoin, and Base ecosystems.

Ecosystem Financing: Polygon wins with star projects, Ethereum and Solana remain hot

Another data point worth noting is financing activity. In 2025, the crypto industry set a new record with 6,710 financing events, categorized by chain. The data shows that the number of financing deals dropped sharply from 640 to 293, but the total amount increased from $350 million to $667 million, with the average deal size rising from $5.57 million to $22.79 million. This indicates that, currently, it is more difficult for small and medium startups to secure funding, while capital is more willing to invest heavily in star projects.

In terms of chain categories, Polygon raised the most with $2.24 billion, followed by Ethereum with $1.57 billion and Solana with $1.34 billion. However, Polygon’s leading position is mainly due to Polymarket’s massive $2 billion+ funding. Looking at the number of financing events, most occurred within the Ethereum, Solana, Bitcoin, and Base ecosystems.

Below is an analysis of several public chains that are key market focuses:

Ethereum: The boat has passed the mountain, fundamentals recover, but token prices stagnate in a “dislocation period”

As the leading public chain, Ethereum’s development in 2025 can be described as “the boat has passed the mountain.” After experiencing ecosystem stagnation caused by severe L2 fragmentation in 2024, and price stagnation, Ethereum saw good growth in ecosystem data in 2025, especially in DEX trading volume (up 38.8%), stablecoin market cap (up 46%), and on-chain active addresses (up 71%). Additionally, in ecosystem financing events and amounts, Ethereum still leads most chains. These indicators suggest that Ethereum’s mainnet ecosystem has recovered in 2025.

However, in terms of price and TVL, the market correction still kept them stagnant. Compared to other chains, ETH’s price performance remains relatively resilient.

Below is an analysis of several public chains that are key market focuses:

Ethereum: The boat has passed the mountain, fundamentals recover, but token prices stagnate in a “dislocation period”

As the leading public chain, Ethereum’s development in 2025 can be described as “the boat has passed the mountain.” After experiencing ecosystem stagnation caused by severe L2 fragmentation in 2024, and price stagnation, Ethereum saw good growth in ecosystem data in 2025, especially in DEX trading volume (up 38.8%), stablecoin market cap (up 46%), and on-chain active addresses (up 71%). Additionally, in ecosystem financing events and amounts, Ethereum still leads most chains. These indicators suggest that Ethereum’s mainnet ecosystem has recovered in 2025.

However, in terms of price and TVL, the market correction still kept them stagnant. Compared to other chains, ETH’s price performance remains relatively resilient.

Solana: Both success and failure with MEME, the fragility after the bubble burst

Compared to 2024, Solana in 2025 shows a different state: the fragility of its ecosystem exposed after big swings. After the MEME market declined at the start of the year, Solana failed to generate further narratives, and instead, various launch platforms continued to compete within the MEME coin track. Although there was significant growth in fee capture and DEX trading volume this year, token prices, active users at year-end, and transaction counts all declined sharply. This also indicates that the market is voting with its feet—Solana’s bubble of prosperity seems to have been burst.

Solana: Both success and failure with MEME, the fragility after the bubble burst

Compared to 2024, Solana in 2025 shows a different state: the fragility of its ecosystem exposed after big swings. After the MEME market declined at the start of the year, Solana failed to generate further narratives, and instead, various launch platforms continued to compete within the MEME coin track. Although there was significant growth in fee capture and DEX trading volume this year, token prices, active users at year-end, and transaction counts all declined sharply. This also indicates that the market is voting with its feet—Solana’s bubble of prosperity seems to have been burst.

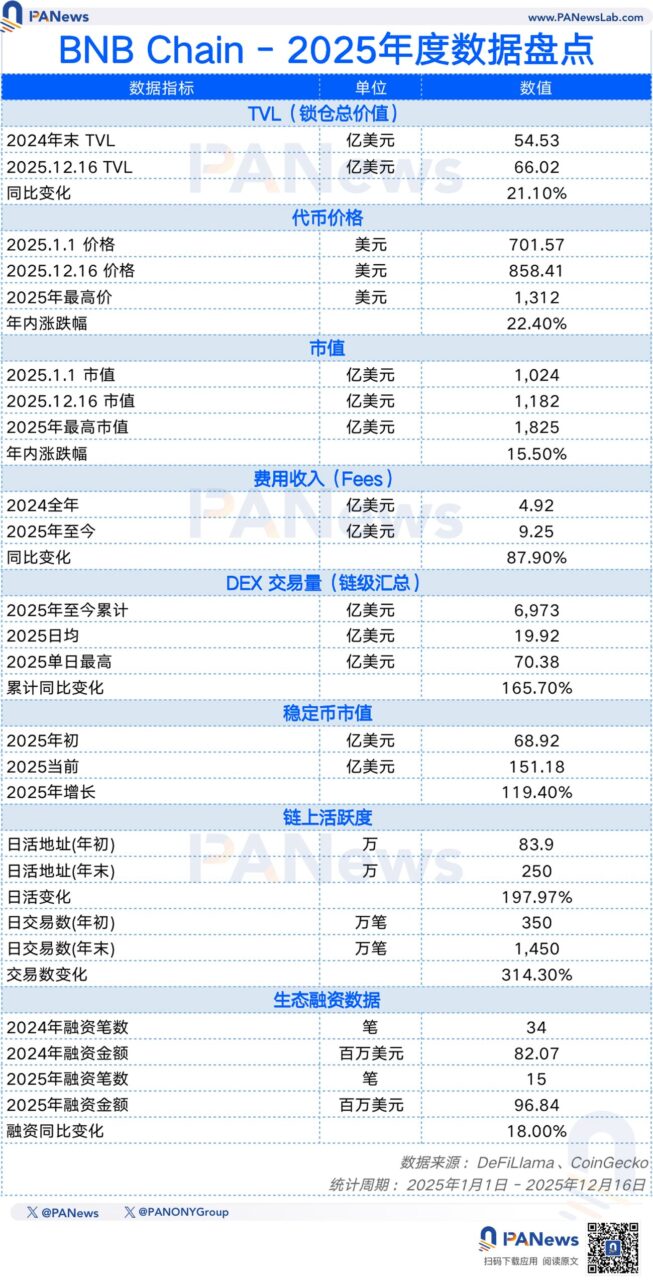

BNB Chain: From defense to full offense, the “hexagonal warrior” with comprehensive growth

BNB Chain experienced a full breakout in 2025, with positive growth across all data dimensions. Especially in fee income, DEX trading volume, stablecoin market cap, and on-chain activity, growth exceeded 100%. Such performance is rare in the context of a sluggish public chain market.

Of course, this success is closely related to Binance. From CZ and other executives actively participating in marketing, to launching Binance Alpha as a “must-have” for retail investors, and new derivatives exchanges like Aster targeting Hyperliquid, BNB Chain’s counterattack in 2024 has turned into a full-scale offensive. This aggressive push makes BNB Chain a formidable opponent that all other chains cannot ignore.

BNB Chain: From defense to full offense, the “hexagonal warrior” with comprehensive growth

BNB Chain experienced a full breakout in 2025, with positive growth across all data dimensions. Especially in fee income, DEX trading volume, stablecoin market cap, and on-chain activity, growth exceeded 100%. Such performance is rare in the context of a sluggish public chain market.

Of course, this success is closely related to Binance. From CZ and other executives actively participating in marketing, to launching Binance Alpha as a “must-have” for retail investors, and new derivatives exchanges like Aster targeting Hyperliquid, BNB Chain’s counterattack in 2024 has turned into a full-scale offensive. This aggressive push makes BNB Chain a formidable opponent that all other chains cannot ignore.

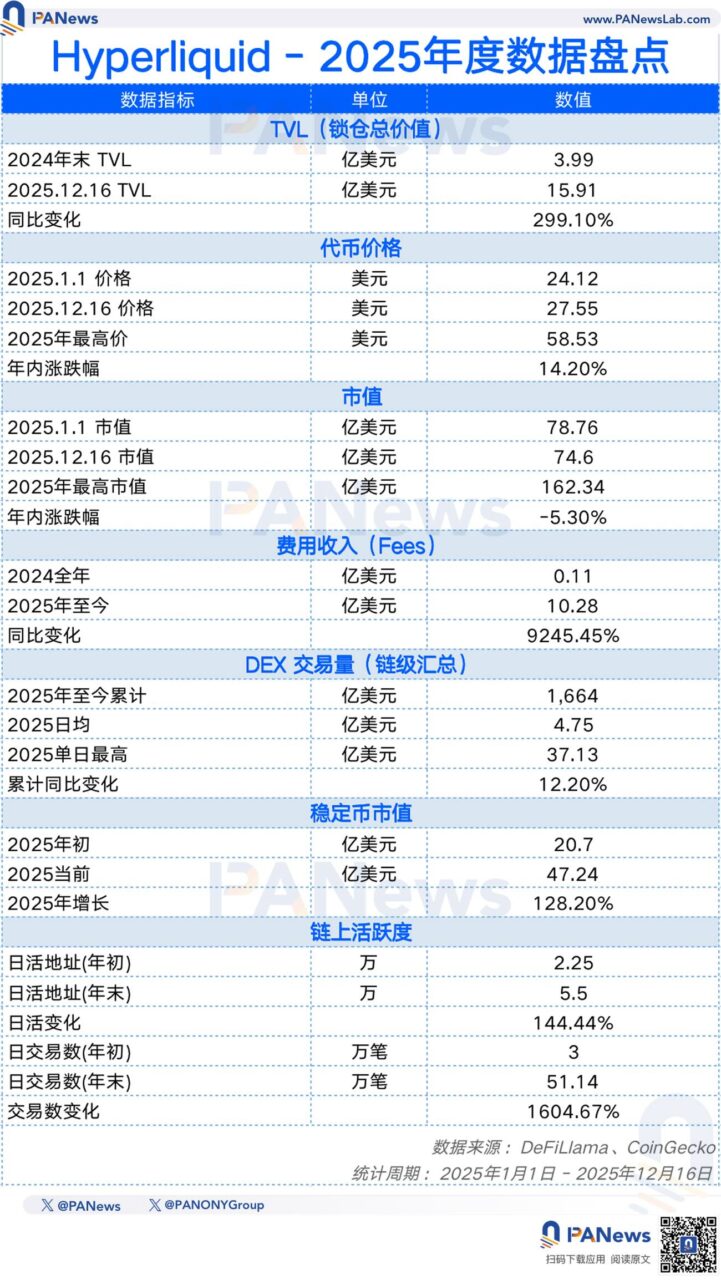

Hyperliquid: The biggest dark horse of the year, teaching the industry a lesson with “real revenue”

Similar to BNB Chain, Hyperliquid also shined brightly in 2025. Aside from a slight decline in market cap (-5.3%) from the start of the year, all other data showed positive growth, with several metrics recording the largest increases among all chains.

In 2025, Hyperliquid ranked ninth in total TVL, third in fee income, sixth in DEX trading volume, and fifth in stablecoin market cap. Based on these rankings, Hyperliquid has become a truly mainstream public chain. As a newcomer to the market, achieving such results is very successful. Moreover, it is one of the few public chains in 2025 that can sustain its ecosystem through genuine revenue without relying on inflation incentives.

However, recently Hyperliquid has faced strong competitors like Aster and Lighter, whose trading volumes are approaching. Unintentionally, Hyperliquid, which was a challenger last year, may have to shift to a defensive stance in 2026.

Hyperliquid: The biggest dark horse of the year, teaching the industry a lesson with “real revenue”

Similar to BNB Chain, Hyperliquid also shined brightly in 2025. Aside from a slight decline in market cap (-5.3%) from the start of the year, all other data showed positive growth, with several metrics recording the largest increases among all chains.

In 2025, Hyperliquid ranked ninth in total TVL, third in fee income, sixth in DEX trading volume, and fifth in stablecoin market cap. Based on these rankings, Hyperliquid has become a truly mainstream public chain. As a newcomer to the market, achieving such results is very successful. Moreover, it is one of the few public chains in 2025 that can sustain its ecosystem through genuine revenue without relying on inflation incentives.

However, recently Hyperliquid has faced strong competitors like Aster and Lighter, whose trading volumes are approaching. Unintentionally, Hyperliquid, which was a challenger last year, may have to shift to a defensive stance in 2026.

Sui: Unlocking the “deep squat” under pressure, awaiting rebirth after the bubble bursts

As a rising chain that in 2024 aggressively caught up with Solana and was highly anticipated by the market, Sui was relatively quiet in 2025. Data shows that Sui’s token price fell by 64%, and TVL dropped by 46.8%, reflecting market pressure. This was mainly due to Sui entering a “mass unlocking period” in 2025. Large amounts of early investor and team tokens entered the market, combined with overall market cooling, leading to price pressure.

Meanwhile, in terms of ecosystem activity, daily active users and daily transaction counts remained almost flat compared to the start of the year, indicating that Sui’s silence this year was rooted in a lack of new narratives and failure to fully explode in the MEME market. However, based on the growth in financing amounts and DEX trading volume, the capital market has not completely abandoned Sui. 2026 may be a year of rebuilding after the bubble burst.

Sui: Unlocking the “deep squat” under pressure, awaiting rebirth after the bubble bursts

As a rising chain that in 2024 aggressively caught up with Solana and was highly anticipated by the market, Sui was relatively quiet in 2025. Data shows that Sui’s token price fell by 64%, and TVL dropped by 46.8%, reflecting market pressure. This was mainly due to Sui entering a “mass unlocking period” in 2025. Large amounts of early investor and team tokens entered the market, combined with overall market cooling, leading to price pressure.

Meanwhile, in terms of ecosystem activity, daily active users and daily transaction counts remained almost flat compared to the start of the year, indicating that Sui’s silence this year was rooted in a lack of new narratives and failure to fully explode in the MEME market. However, based on the growth in financing amounts and DEX trading volume, the capital market has not completely abandoned Sui. 2026 may be a year of rebuilding after the bubble burst.

Tron: The ultimate pragmatist, the “cash flow king” deep in the payments track

In 2025, Tron’s development set a new narrative for the public chain market: leveraging stablecoins to continue “quietly making money.” Although TVL and token prices declined by about half, Tron still generated $184 million in on-chain fees (up 126.9%) and expanded DEX trading volume by 224%. For Tron, rather than chasing hot topics and creating new narratives, it’s better to focus on solid fundamentals like global stablecoin settlement. This pragmatic approach has made Tron a public chain with stable cash flow and strong user stickiness.

Tron: The ultimate pragmatist, the “cash flow king” deep in the payments track

In 2025, Tron’s development set a new narrative for the public chain market: leveraging stablecoins to continue “quietly making money.” Although TVL and token prices declined by about half, Tron still generated $184 million in on-chain fees (up 126.9%) and expanded DEX trading volume by 224%. For Tron, rather than chasing hot topics and creating new narratives, it’s better to focus on solid fundamentals like global stablecoin settlement. This pragmatic approach has made Tron a public chain with stable cash flow and strong user stickiness.

Looking back at the public chain landscape of 2025, it’s not just a report card but a reflection of the diverse development of the industry.

Looking back at the public chain landscape of 2025, it’s not just a report card but a reflection of the diverse development of the industry.

The clear red and black list of data tells us: the era of “thousands of horses galloping” in the public chain track has ended, replaced by a brutal “stock competition” and “oligopoly” trend. Whether it’s Solana’s traffic anxiety after the MEME craze, Sui’s price pain under token unlocks, or the disastrous secondary market performance of new chains like Movement and Scroll, all prove that the false prosperity maintained by VC funding and PUA tactics is no longer sustainable.

However, amid the widespread decline, we can see the evolution of industry resilience. BNB Chain’s explosive ecosystem growth, Hyperliquid’s reliance on genuine revenue, and Tron’s pragmatic focus on payments collectively point to the survival rules for 2026: survive, not by storytelling, but by making money; not by volume manipulation, but by real users.

The cold winter of 2025 may be biting, but it has successfully squeezed out the bubbles attached to public chains for years. Looking forward to 2026, we have reason to believe that on this cleaner, more pragmatic foundation, public chains will no longer be just gambling casinos but will truly become the global infrastructure for large-scale value exchange.

The clear red and black list of data tells us: the era of “thousands of horses galloping” in the public chain track has ended, replaced by a brutal “stock competition” and “oligopoly” trend. Whether it’s Solana’s traffic anxiety after the MEME craze, Sui’s price pain under token unlocks, or the disastrous secondary market performance of new chains like Movement and Scroll, all prove that the false prosperity maintained by VC funding and PUA tactics is no longer sustainable.

However, amid the widespread decline, we can see the evolution of industry resilience. BNB Chain’s explosive ecosystem growth, Hyperliquid’s reliance on genuine revenue, and Tron’s pragmatic focus on payments collectively point to the survival rules for 2026: survive, not by storytelling, but by making money; not by volume manipulation, but by real users.

The cold winter of 2025 may be biting, but it has successfully squeezed out the bubbles attached to public chains for years. Looking forward to 2026, we have reason to believe that on this cleaner, more pragmatic foundation, public chains will no longer be just gambling casinos but will truly become the global infrastructure for large-scale value exchange.