Since the US-Israel-Iran war broke out on February 28, 2026, the Strait of Hormuz has been mired in shipping disruption for more than four and a half months. On July 7, the US military launched a new round of strikes on Iran, citing the “Iranian threat to navigation by merchant vessels through the Strait of Hormuz.” On July 12, Iran announced a blockade of the Strait of Hormuz. On July 13, US President Trump announced that the US would restore its maritime blockade of Iran. On July 14, the US military completed strikes on dozens of military targets near the Strait of Hormuz and along Iran’s coastline. By the night of July 14, the US-Iran confrontation was still ongoing. Around what is arguably the world’s most critical energy transportation corridor, military standoff has shifted from intermittent clashes to sustained conflict.

What the current market is facing is no longer simple short-term oil price volatility, but a complete transmission chain consisting of supply risk → falling inventories → expansion of risk premium → oil price re-pricing. This article will break down this logic from three dimensions: the strategic position of the Strait of Hormuz, the current state of consumption of global strategic petroleum reserves, and the realism of $100 oil.

The “throat” of global oil transport: Why the Strait of Hormuz is irreplaceable

The Strait of Hormuz connects the Persian Gulf and the Indian Ocean, and is the only seaborne route for crude oil exports from Gulf oil-producing countries such as Saudi Arabia, the UAE, Kuwait, Qatar, and Iraq. In normal times, about 20 million barrels of oil and oil products pass through the strait each day, accounting for roughly one-quarter of global seaborne crude oil trade. About 80% of that volume is bound for Asia. From a more macro perspective, the strait carries about 35% of global crude oil trade and 20% of global crude oil supply, with 90% delivered to the Asian market. In addition, about one-fifth of global LNG trade also depends on this corridor.

The meaning of these figures is very direct: the operability of the Strait of Hormuz directly determines whether roughly one-fifth of global daily crude oil can reach consumer markets smoothly. Even if Saudi Arabia and the UAE have pipelines that can bypass the strait, their combined real diverting capacity totals only about 3.5 million to 5.5 million barrels per day—far from being able to replace the strait’s normal daily transport volume of 20 million barrels. Routing via pipelines can only cover a small portion of the strait’s normal throughput, and the bypass routes themselves also face geopolitical risks in the direction of the Red Sea.

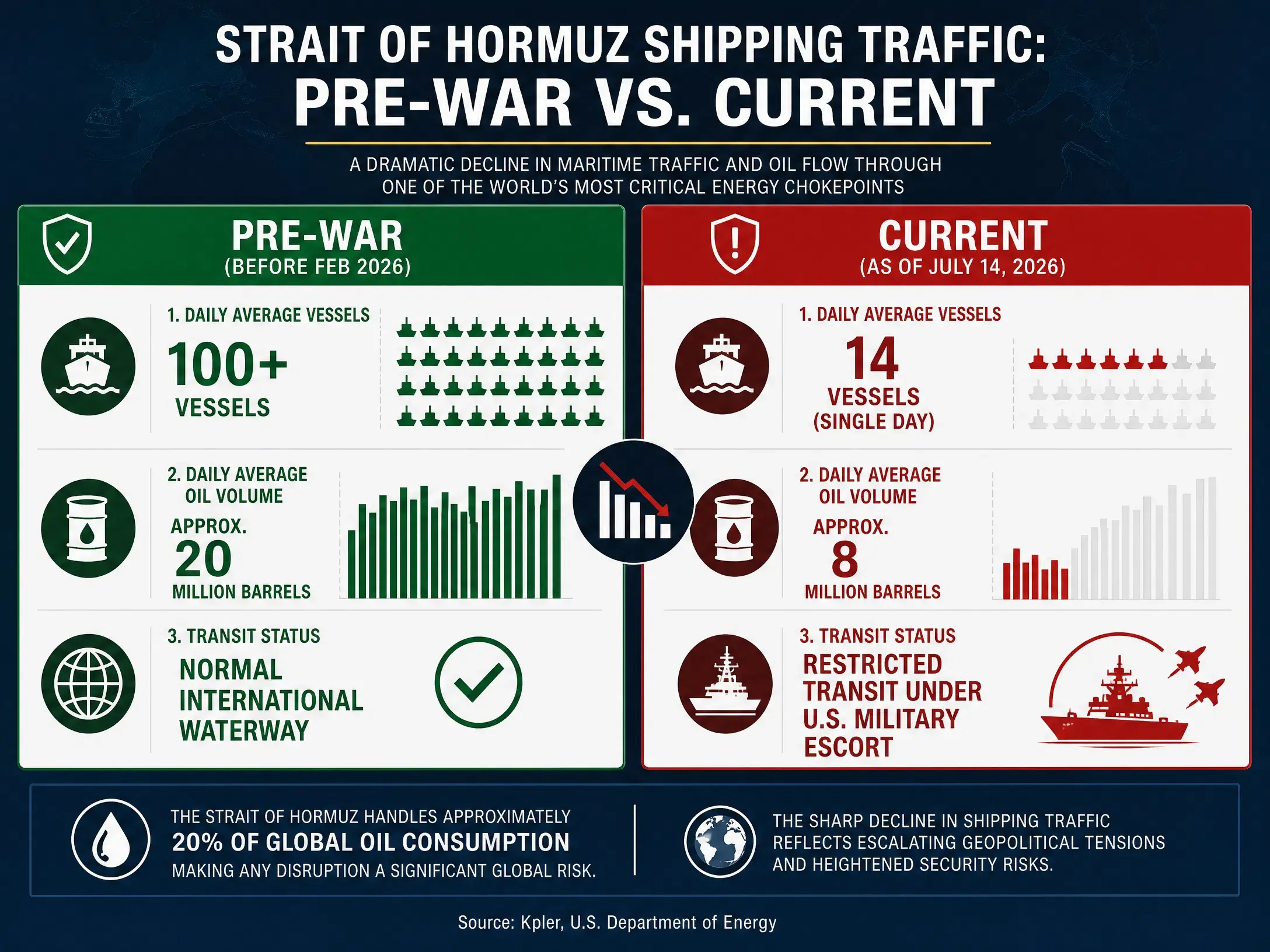

After Iran blocked the Strait of Hormuz at the end of February 2026, Middle East crude export volumes dropped sharply from about 15 million barrels per day before the conflict. Even though there were several temporary ceasefires and partial resumption of navigation after that, shipping data has never returned to normal. In June, the average number of vessels transiting the Strait of Hormuz was only around 60% of the usual scale of normal passage. In a research report, ING noted that the surge in currently passing vessels is almost entirely made up of tankers that had been stranded in the Persian Gulf after the blockade earlier; they represent a one-time release of stranded transport capacity. The number of tankers sailing into the Persian Gulf to load cargo at crude oil ports remains at a historically low level. On July 9, the Strait of Hormuz passage volume fell to 25 ships, below the recent daily average of 30 to 50 ships.

This means that even during conflict lulls, the Strait of Hormuz’s energy transport function has not recovered to pre-war levels. And since July, the renewed escalation of the US-Iran military standoff has shattered any lingering expectations of “returning to normal.”

Comparison of changes in Strait of Hormuz passage volumes

Strategic oil reserves’ “cushion” is thinning

Against the backdrop of impeded passage through the Strait of Hormuz, the world’s last line of defense for buffering supply shocks in the global crude oil market—strategic petroleum reserves—is being consumed at an astonishing pace.

On March 11, 2026, 32 member countries of the International Energy Agency agreed unanimously to release 400 million barrels of emergency oil to the global market—the largest coordinated intervention since the IEA was founded 52 years ago. The United States accounted for a release share of 172 million barrels.

However, even this unprecedented scale of reserve releases failed to change the fundamental situation of tight supply and demand. The latest data from the US Department of Energy shows that in the week ending July 3, US strategic petroleum reserves fell sharply by 6.2 million barrels, bringing total inventory to 319.5 million barrels— the lowest level since April 1983. Other data show that SPR has dropped to 316.5 million barrels. As of July 3, US total crude oil inventories (including commercial inventories and strategic reserves) fell to 730.8 million barrels, the lowest level since 1984.

Over a longer period, under the policy of successive US administrations using reserves to smooth out oil prices, US strategic petroleum reserves have cumulatively decreased by 352 million barrels. Of the IEA’s planned release of 400 million barrels, 271.7 million barrels comes from government reserves of member countries, while 116.6 million barrels comes from industry reserves. By mid-July, the US had already used about 98.9 million barrels.

A continued decline in strategic oil reserves means that the market’s buffering space for sudden supply disruptions is narrowing. Previously, whenever oil prices surged due to geopolitical events, the US and IEA member countries could temper prices in the short term by releasing reserves. But when reserves themselves are already at the lowest levels in decades, the effectiveness of this policy tool is greatly reduced. The market’s pricing logic is undergoing fundamental change—reserves are no longer a “stabilizer that can be used anytime,” but rather a “scarce asset that is being consumed quickly and is difficult to replenish rapidly.”

The IEA had previously warned that even if a temporary US-Iran agreement is implemented, the main shipping routes still need to clear mines, and stranded vessels, port loading and unloading, refinery procurement, and supply chain arrangements also need to be reconnected. And now, the renewed escalation of mutual attacks between the US and Iran has called the temporary agreement’s effectiveness into question at its core.

Structural amplification of supply risk: from a gap to a risk premium

The key to understanding the current oil price trajectory is to distinguish between “upward moves driven by demand” and “upward moves driven by supply risk.” The core driving force of this round of oil price fluctuations is not demand expansion driven by global economic growth, but supply disruption risk triggered by impeded passage through the Strait of Hormuz.

From the supply-demand fundamentals, the EIA expects a global crude oil supply-demand gap of about 3.87 million barrels per day in 2026. CICC expects global oil supply to fall year-on-year by about 4.3% for the full year, demand to decline year-on-year by about 1.0%, and the supply-demand shortfall to be about 2.04 million barrels per day. Another institution estimates that in June, global oil supply rose by 4.1 million barrels per day as the strait reopened, but compared with pre-war levels, the gap is still as high as 9.4 million barrels per day. The IEA had previously predicted that the global oil market would run a deficit of 1.78 million barrels per day in 2026.

These figures point to the same conclusion: even without considering further deterioration in the Strait of Hormuz, the global crude oil market was already in a supply-tight state in 2026. The fact that passage through the strait is impeded is pushing that already tight state into a more severe imbalance.

Another structural feature of the supply gap is regional imbalance. The restricted export volume of crude oil from the Persian Gulf area is close to 10 million barrels per day. China’s share of imports from the Persian Gulf is about 53%, Korea’s is 64%, and Japan’s is 75%. This means the supply shortfall is concentrated mainly in the Asian market, while the reserves released by the IEA mostly come from Europe and the United States. The voyage distance from the Atlantic to the Far East is about 14,000 to 15,000 nautical miles—about 2.5 times that of the Middle East-to-Far East route. The longer transport distance not only increases shipping costs but also extends the time it takes for supply to recover.

The structural feature of supply risk also appears in the absolute level of inventories. Some analysis suggests that if the strait remains blocked and the drawdown speed in April is maintained, global crude oil inventories could reach the operational pressure line (about 7.6 billion barrels) in June, and the operational bottom line (about 6.8 billion barrels) in November. While the actual drawdown pace may slow due to demand destruction, the risk of inventories approaching the operational bottom is being gradually priced in by the market.

Is $100 oil realistic: key variables and institutional expectations

Returning to the core question: after global crude oil markets have already experienced violent swings from below $70 per barrel to a brief break above $114, is $100 per barrel a reasonable expectation in the current environment, or excessive panic?

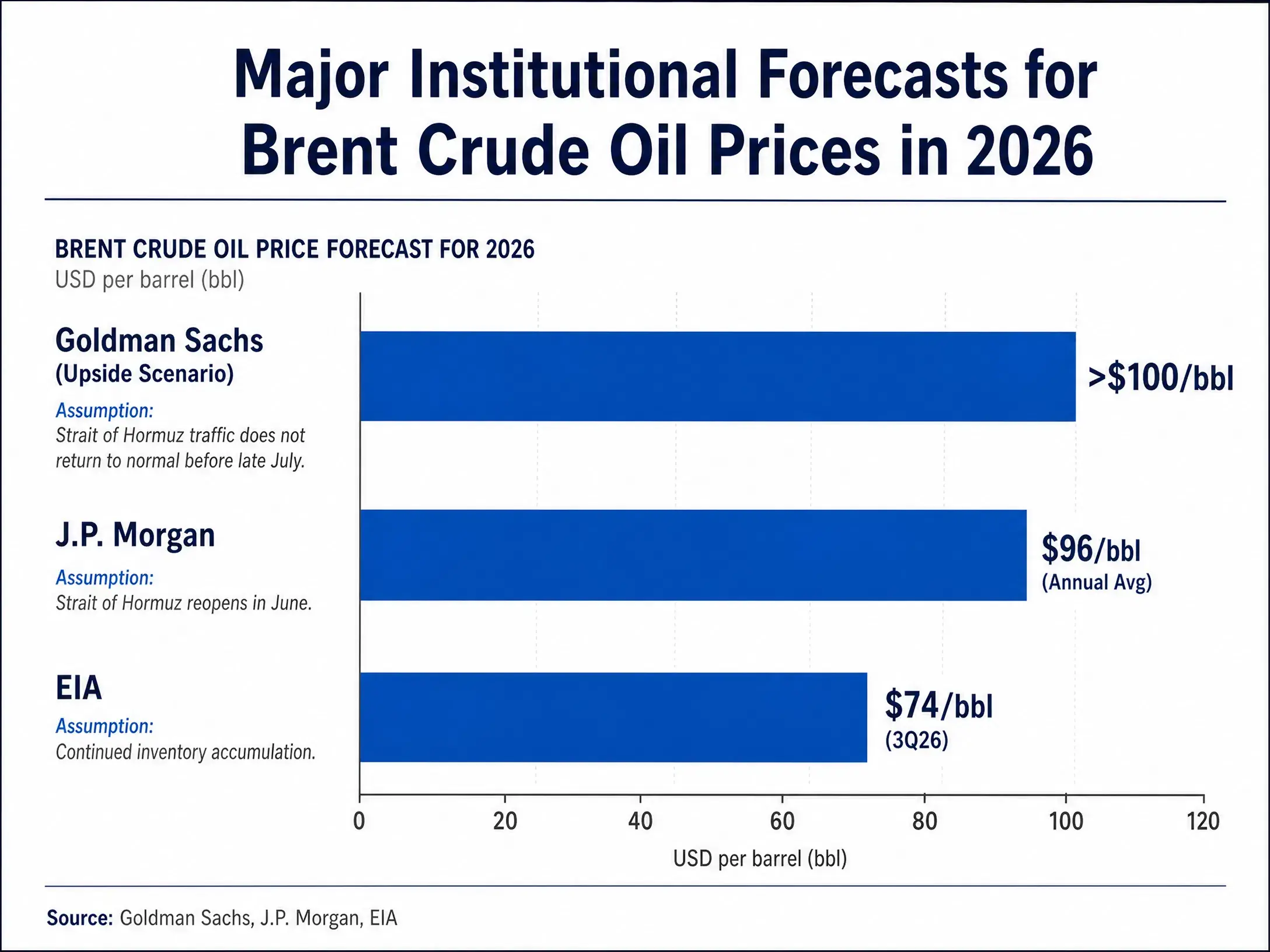

From institutional forecasts, there are clear disagreements among mainstream investment banks, but there is also a certain consensus range. In its March analysis, Goldman Sachs said that whether in the short term or in 2027, oil price risk remains tilted to the upside; ongoing multiple historical large-scale supply disruptions highlight the risk that oil prices could remain above $100 per barrel for a long time. Goldman’s baseline scenario assumes that if April flows recover gradually, Brent crude prices will fall back to the $70s per barrel in the fourth quarter of 2026. In the bull scenario, Goldman expects oil prices to rise to around $100 per barrel.

JPMorgan’s view is more hawkish. The firm’s head of global commodities research said that even if the Strait of Hormuz reopens in June, oil prices are expected to stay above $100 per barrel through the end of 2026. JPMorgan expects oil prices in the second quarter to remain at elevated levels above $100. Other analysis notes that if by the end of 2026 the Brent crude price reaches $90 per barrel, global economic growth will slow; if it climbs further to more than $150 per barrel, it would directly lead to a global recession.

The IMF’s baseline forecast assumes Brent averages $82 in 2026, but its adverse scenario—if the conflict persists—puts the oil price at $100 and global growth slowing. In its latest forecast in July, the EIA is relatively conservative, expecting Brent to average $74 per barrel in the third quarter of 2026.

Comparison of major institutions’ 2026 oil price forecasts

Overall, $100 per barrel is not beyond reach, but it requires specific conditions. These include: continued impeded passage through the Strait of Hormuz or a renewed comprehensive blockade; strategic petroleum reserves being further depleted to a truly low level; OPEC+ and other oil-producing countries’ production increases failing to effectively make up for the supply shortfall; and no major demand-side contraction sufficient to offset the supply shock.

Three key variables determine the direction of oil prices

The current question of whether oil prices can break above $100 and hold at high levels can be summarized into three interconnected key variables.

First, whether Iran will further escalate its blockade actions against the strait. On July 12, Iran announced a blockade of the Strait of Hormuz, while the US military insists that the strait remains open. The struggle between both sides over control of strait management is shifting from verbal sparring to substantive military confrontation. Iran’s parliament has drafted new legislation to control the strait, while the US military has restored a maritime blockade of Iran. If Iran takes more aggressive blockade measures—for example, laying mines in the shipping lanes, and systematically intercepting and seizing passing tankers—passage through the strait could slide directly from “restricted” to “interrupted.” If that happens, the transport of 20 million barrels of oil per day would face a material standstill, and oil prices could break above $100 within an extremely short time.

Second, whether the US expands the scope and intensity of its military actions. On July 14, the US military completed strikes on dozens of military targets near the Strait of Hormuz. More than 20 US naval vessels and hundreds of military aircraft are carrying out missions in the Middle East. If the US escalates its military actions from “striking military targets” to “a comprehensive blockade of Iran’s oil exports,” or even “striking Iran’s domestic energy infrastructure,” the nature of the conflict would change fundamentally. That would not only push up the risk premium directly but could also trigger Iran’s retaliatory strikes against facilities in other Gulf oil-producing countries, causing multiple shocks on the supply side.

Third, the pace of depletion of global strategic oil reserves and the capacity to replenish them. Currently, the US SPR has fallen to the lowest level since 1983. If the conflict continues, further depletion of reserves will be unavoidable. When reserves fall near the operational bottom line, the market will have to face a reality: the energy security buffer mechanisms built over the past decades may be completely exhausted in this round of crisis. The irreversible decline of reserves means that any new supply shock will be transmitted directly to prices, with no longer enough buffering space in between.

From short-term volatility to structural re-pricing

The impact of the current Strait of Hormuz crisis on the global crude oil market is evolving from “short-term volatility” into “structural re-pricing.”

In terms of market pricing mechanisms, earlier oil prices fell quickly on negotiation progress and rebounded swiftly as the conflict escalated, indicating that the core of market pricing is not the number of daily transiting vessels, but rather the sustainability of the ceasefire situation and the possibility of risk-driven rebounds. Current transits are essentially “conditional”—highly dependent on temporary ceasefire arrangements, navigation safety relies on bilateral communication mechanisms, and commercial operations rely on additional insurance coverage. When these added constraints collapse due to military conflict, the market’s risk pricing will be recalibrated.

Over a longer cycle, the passage risk of the Strait of Hormuz is shifting from a “one-off event” to a “persistent premium.” The US and Iran’s game over control of the strait has expanded beyond mere military confrontation into a competition over institutions at the legislative level. The US has announced it will be known as the “Strait of Hormuz Guardian,” while Iran has proposed a bill for the “Strategic Action Plan for the Strait of Hormuz and the Security and Sustainable Process of the Persian Gulf.” This institutional-level competition means that even if the current military conflict temporarily calms down, the rules and cost structure for passage through the strait may change permanently.

For the global crude oil market, this means geopolitical risk premium may not fully disappear as the conflict temporarily eases. The market will have to price in an operating environment for the Strait of Hormuz characterized by “higher risk and higher costs.” In this context, the $80 to $100 range could become a new normal volatility band, and any new escalation of conflict would push prices to break through $100—possibly to even higher levels.

FAQ

Q1: How important is the Strait of Hormuz to the global crude oil market?

The Strait of Hormuz is the world’s most critical energy transportation corridor. In normal times, about 20 million barrels of oil pass through it each day, accounting for one-quarter of global seaborne crude oil trade and one-fifth of global crude oil supply. Crude oil exports from major producing countries such as Saudi Arabia, the UAE, Kuwait, and Qatar rely almost entirely on this strait. Its operating status directly determines whether one-fifth of global daily crude oil can reach consumption markets smoothly.

Q2: Why have US strategic oil reserves fallen to historical lows?

As of July 3, 2026, US SPR has dropped to 319.5 million barrels, the lowest level since April 1983. The decline mainly results from the US government’s plan to release 172 million barrels of crude oil to address supply shortages caused by the Iran war; about 98.9 million barrels have been used so far. Under policies of successive administrations using reserves to smooth oil prices, the US strategic petroleum reserves have cumulatively decreased by 352 million barrels.

Q3: Will oil prices really rise to $100?

$100 is possible but requires specific conditions: continued impeded or fully blocked passage through the Strait of Hormuz; further depletion of strategic petroleum reserves; and OPEC+ and other producers’ output failing to effectively compensate for the supply shortfall. Goldman Sachs suggests prices could remain above $100 long-term, JPMorgan expects prices to stay above $100 through 2026, while the EIA’s forecast is more conservative, with an average Brent of $74 in Q3 2026.

Q4: Is the recent rise in oil prices driven by demand or supply risk?

The primary driver is supply disruption risk, not demand growth. The expected global supply-demand gap in 2026 is about 3.87 million barrels per day, with the Strait blockade sharply reducing Middle East exports. The market is pricing in the risk premium of potential supply interruptions, not actual demand expansion.

Q5: Can OPEC+ production increases prevent further price rises?

OPEC+ plans to raise output by 188,000 barrels per day in August, but this is very limited compared to the roughly 20 million barrels per day potential disruption at the Strait of Hormuz. Even with additional increases from non-OPEC producers like the US and Brazil (~1.15 million barrels per day in 2026), it would still fall short of fully offsetting the supply shortfall caused by a comprehensive blockade.