President Donald Trump renewed his campaign pledge on January 9, 2026 (U.S. Eastern Time), urging that credit card interest rates be capped at a maximum of 10% for a one-year period beginning January 20, 2026—the one-year anniversary of his second inauguration.

(Sources: X)

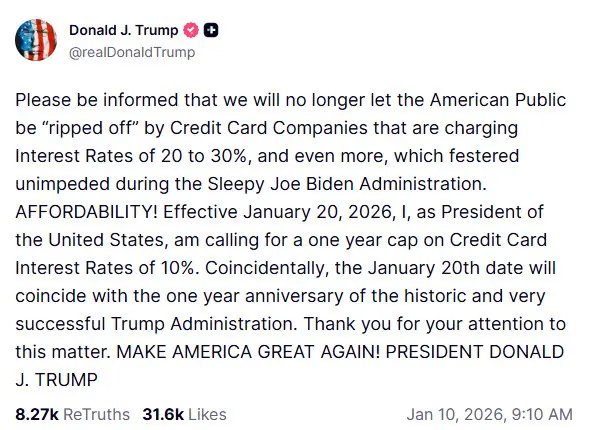

In a post on his Truth Social platform, Trump described current rates of 20–30% or higher as “exploitation” and “slaughter” of American consumers, claiming the issue was ignored under the previous Biden administration. He vowed to end the practice, stating: “We will no longer allow the American people to be gouged by credit card companies.”

The announcement has reignited debate over Trump credit card interest cap policy, with bipartisan support in Congress for similar measures but widespread skepticism about implementation without legislative action. Major banks and industry groups quickly pushed back, warning of reduced credit availability and higher costs for consumers.

Trump’s Proposal: 10% Cap for One Year

Trump’s call for a credit card interest cap of 10% echoes a promise made during his successful 2024 presidential campaign. In his January 10 post, he emphasized that high rates burden everyday Americans who rely on credit cards for essential expenses, especially amid lingering inflationary pressures.

- Proposed Effective Date: January 20, 2026 (coinciding with the one-year mark of his second term).

- Duration: One year.

- Rationale: Described as stopping “exploitation” and protecting household finances.

- Execution Details: No specific mechanism provided—Trump did not reference any particular bill or executive action pathway.

Analysts have long noted that setting a national credit card interest cap would almost certainly require Congressional legislation, as the Federal Reserve and executive branch lack direct authority to impose binding rate ceilings on private lenders.

Bipartisan Congressional Interest Meets Political Reality

Both Democrats and Republicans have previously expressed concern over high credit card rates:

- Sen. Bernie Sanders (D-VT) and Sen. Josh Hawley (R-MO) co-sponsored bipartisan legislation proposing a 10% cap for five years.

- Rep. Alexandria Ocasio-Cortez (D-NY) and Rep. Anna Paulina Luna (R-FL) introduced a companion House bill with the same 10% ceiling.

Despite this cross-party interest, no such legislation has become law. Sen. Elizabeth Warren (D-MA), a longtime advocate for stricter credit card rules, criticized Trump’s announcement as “meaningless” without Congressional passage. Warren noted her willingness to work with Trump on the issue but highlighted previous attempts by his administration to weaken the Consumer Financial Protection Bureau (CFPB).

Trump’s post did not explicitly endorse any specific pending bill, leaving open questions about how the cap would be enforced.

Industry Response: Warnings of Reduced Credit Supply

Major U.S. credit card issuers—including American Express, Capital One, JPMorgan Chase, Citigroup, and Bank of America—did not immediately respond to requests for comment. However, key industry associations issued a joint statement warning that a 10% credit card interest cap would “reduce the supply of credit” and “push consumers toward less regulated, higher-cost alternatives.”

The Consumer Bankers Association and American Bankers Association argued that such a cap would make many current cardholders—particularly those with lower credit scores—unprofitable for issuers, leading to tighter lending standards, reduced credit limits, or outright account closures.

- Industry View: Caps distort risk pricing and shrink access.

- Consumer Impact: Potentially higher costs via fees or alternative lenders.

- Historical Precedent: Previous attempts at rate caps have faced similar pushback.

Trump Administration’s Prior Actions on Credit Card Fees

The current proposal follows the Trump administration’s successful effort to overturn a Biden-era CFPB rule that would have capped credit card late fees at $8. The administration challenged the rule in federal court, arguing it was unlawful, and a judge ultimately vacated the provision.

This history has fueled criticism that Trump’s new call for a credit card interest cap may face similar legal and political hurdles without clear Congressional backing.

Outlook: Political Pressure vs. Legislative Reality

Trump’s announcement aligns with ongoing voter frustration over rising living costs and debt burdens, especially as midterm elections approach in November 2026. The timing—coinciding with his administration’s one-year anniversary—appears designed to project action on a pocketbook issue.

However, without a specific bill or executive pathway, the proposal remains aspirational. Industry opposition, constitutional questions about executive authority over private lending rates, and the need for bipartisan support in Congress suggest implementation faces significant obstacles.

In summary, President Trump’s call for a credit card interest cap of 10% starting January 20, 2026, revives a 2024 campaign promise but lacks detailed execution plans and faces immediate skepticism from lawmakers and sharp pushback from the banking industry. While bipartisan concern over high credit card rates exists—evidenced by prior legislative proposals—the move requires Congressional authorization to become binding. The announcement reflects political pressure to address consumer debt burdens but highlights the challenges of imposing rate ceilings on private lenders in a market-driven economy. Investors and consumers should monitor any formal legislative proposals or executive actions for clarity—always reference official White House, Congressional, and regulatory sources for developments related to credit card policy.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.