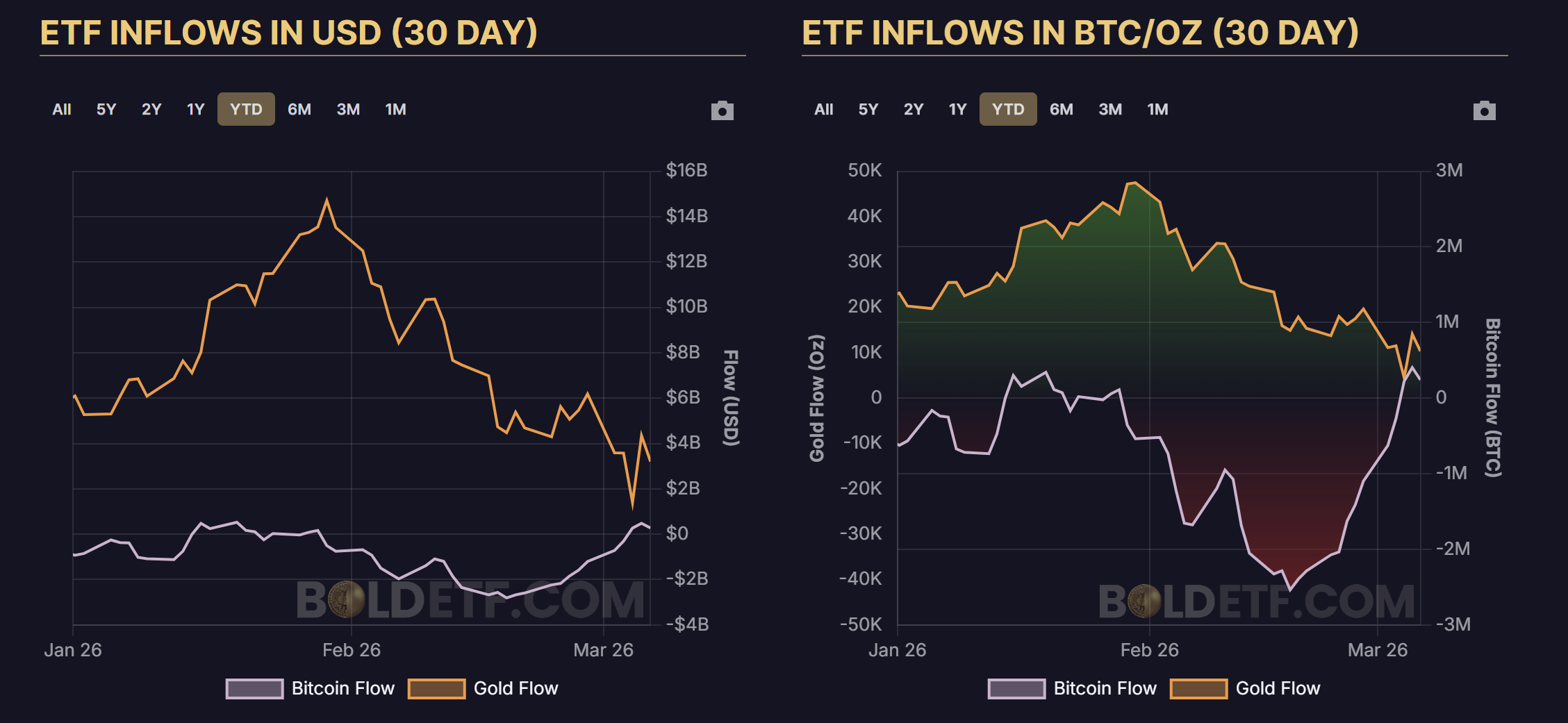

The largest U.S. gold ETF (GLD) experienced a $3 billion outflow on Wednesday, marking the biggest single-day redemption in over two years, while gold prices declined by 4.4% during the same period. Meanwhile, the 30-day net inflow for Bitcoin ETFs reversed from -$1.9 billion on February 6 to +$273 million on March 6, indicating a stark contrast in capital flows between the two asset classes.

Contrasting Signals in ETF Capital Flows: Gold Outflows, Bitcoin Inflows

(Source: Bold Report)

(Source: Bold Report)

Gold ETFs began 2026 with their strongest start on record: attracting $18.7 billion in January and another $5.3 billion in February, continuing a nine-month streak of capital inflows. The recent large-scale outflows suggest investors are taking profits after gold prices surged significantly since 2025.

Measured in native units, the divergence in capital flows becomes clearer. Bitcoin ETF holdings increased from -42,275 BTC on February 6 to +4,021 BTC on March 6, reflecting actual accumulation of assets; during the same period, gold holdings in gold ETFs decreased from 1.4 million ounces to 621,100 ounces, a reduction of over half. Tracking in native units (BTC count, ounces) rather than dollar value removes distortions caused by price fluctuations, providing a more accurate picture of actual capital movement.

Historical Rotation Cycle: 147-Day Pattern of Bitcoin Surpassing Gold

(Source: Trading View)

(Source: Trading View)

Fidelity Digital Assets analyst Chris Kuiper, in their December 2025 “2026 Outlook” report, noted that gold’s 65% return in 2025 was the fourth-highest annual gain since the end of the gold standard, and based on historical rotation patterns, he stated: “Historically, gold and Bitcoin tend to perform alternately. Given gold’s stellar performance in 2025, it wouldn’t be surprising if Bitcoin takes the lead next.”

Historical technical data provides a specific timeframe for this:

-

Consolidation Phase (0-147 days): After Bitcoin bottomed in 2022, it required about 147 days (21 weeks) of consolidation, with no clear trend of consistently outperforming gold yet established.

-

Transition Phase (after 21 weeks): The Bitcoin-to-gold ratio began to rise significantly, entering a period of Bitcoin relative strength.

Currently, the Bitcoin-to-gold ratio is oscillating near the same consolidation zone seen in early 2022-2023, which some analysts view as a typical pattern before a rotation trigger.

Multi-Dimensional Analyst Perspectives: Ongoing Geopolitical Asset Effects

Joe Consorti points out that the U.S. economy’s accelerated growth and improved market risk sentiment could lead Bitcoin to outperform gold in the near term, suggesting “a shift from safe-haven to risk-on assets may already be underway.”

Chris Kuiper adds that persistent fiscal deficits, trade tensions, and geopolitical uncertainties—including ongoing U.S.-Israel-Iran conflicts—may benefit both assets simultaneously, as investors seek neutral stores of value outside traditional fiat systems. Macro strategist Lyn Alden predicts that after gold’s strong recent performance, Bitcoin will outperform gold over the next two to three years.

All these analyses are based on historical pattern frameworks; actual market rotation timing and magnitude are influenced by multiple macro factors and carry considerable uncertainty.

Frequently Asked Questions

What is the main reason behind the record-breaking outflows from gold ETFs?

The $3 billion single-day redemption in GLD reflects investors taking profits after significant gold price increases. The nine consecutive months of inflows into gold ETFs at the start of 2026 set a record, and the subsequent large-scale redemptions indicate capital is reallocating from high-positioned gold holdings to other assets.

How long do historical rotation cycles between Bitcoin and gold typically last?

Based on 2022-2023 data, Bitcoin usually requires about 147 days (21 weeks) of consolidation after bottoming before establishing a trend of outperforming gold. The current Bitcoin-to-gold ratio’s technical position is similar to early rotation phases, but past patterns do not guarantee future outcomes.

Why do analysts remain optimistic about the long-term prospects of both Bitcoin and gold?

Fidelity analyst Chris Kuiper notes that ongoing fiscal deficits, trade tensions, and geopolitical uncertainties benefit both assets as neutral stores of value outside the traditional monetary system. While their leading cycles may alternate, both assets have structural demand in macroeconomic uncertainty environments.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.