#BernsteinSaysMemoryBullMarketToLastUntil2027

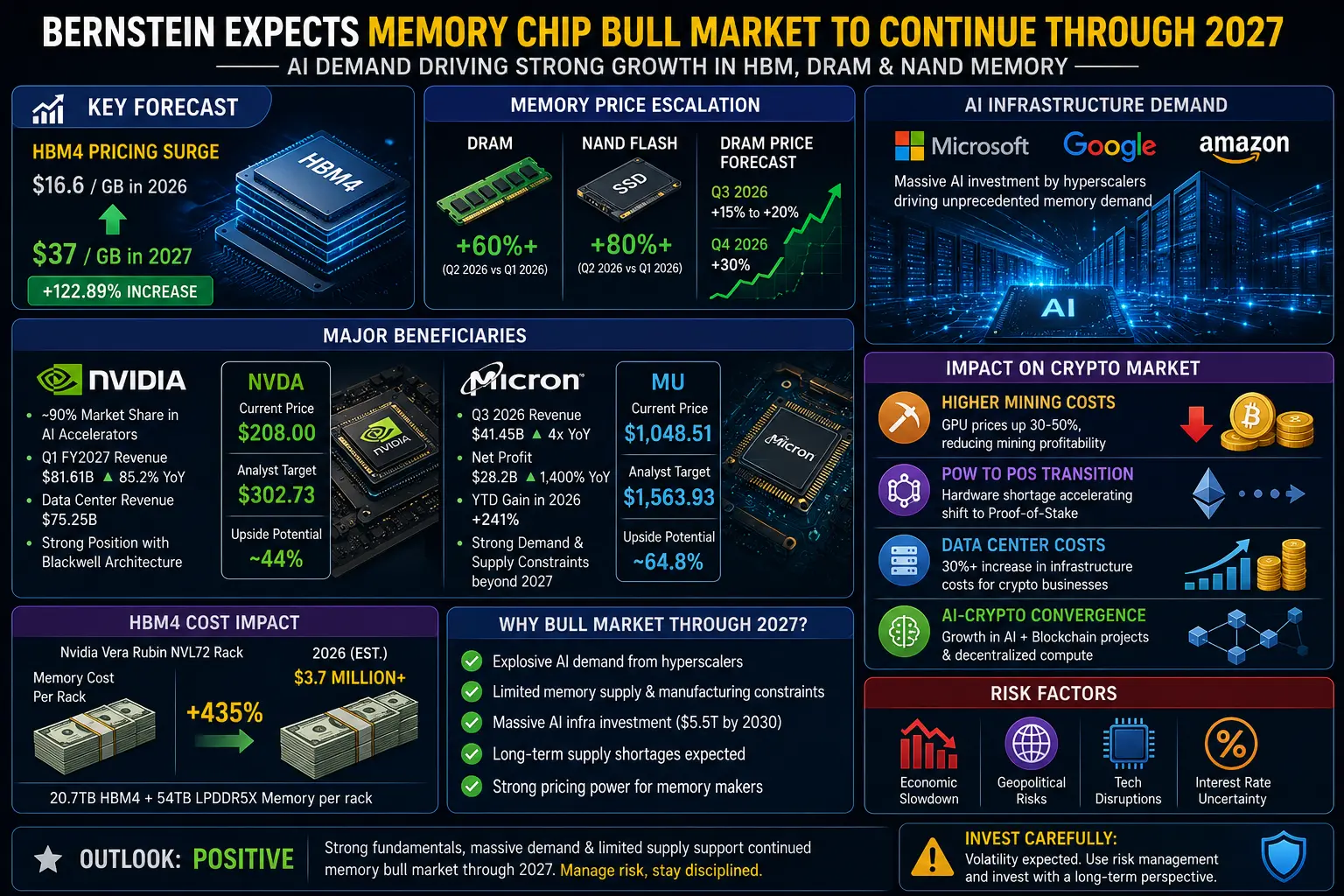

Bernstein, a leading global investment research and asset management firm, has issued a bold prediction that the memory chip bull market will extend through 2027, driven by unprecedented demand from artificial intelligence infrastructure, data centers, and high-performance computing applications. This forecast represents a significant bullish signal for major memory chip manufacturers including SK Hynix, Samsung Electronics, and Micron Technology, indicating that the current uptrend in the semiconductor sector has substantial runway ahead.

The memory chip industry has experienced a remarkable transformation over the past eighteen months, evolving from a cyclical commodity business into a critical enabler of the AI revolution. High-Bandwidth Memory (HBM) chips have emerged as the most sought-after components in the semiconductor supply chain, with demand significantly outpacing available manufacturing capacity. SK Hynix currently dominates the HBM market with approximately 58% global market share, substantially ahead of Micron's 21% market share. This leadership position has positioned SK Hynix as the primary beneficiary of the AI infrastructure buildout, with Bernstein projecting that the company will achieve gross margins of 91% by the second quarter of 2026, accompanied by operating margins between 70% and 80%. These figures compare favorably to Micron's projected operating margins of 50% to 55%, highlighting SK Hynix's superior competitive positioning in the high-margin HBM segment.

Micron Technology has also demonstrated exceptional performance, with the company reporting record quarterly revenue of $41.46 billion and adjusted gross margins reaching 84.6%. The company has secured approximately $100 billion in contracted multi-year revenue through non-cancelable, take-or-pay agreements, effectively insulating its business from the traditional boom-bust cycles that have historically characterized the DRAM industry. Micron has committed up to $3 billion toward domestic expansion initiatives, including $500 million in strategic financing to GlobalWafers to support its Sherman, Texas facility, alongside a ten-year silicon wafer supply agreement that locks in raw material capacity for the foreseeable future. The company's HBM supply has been completely sold out through 2028, underscoring the structural supply-demand imbalance that continues to drive pricing power across the memory chip sector.

Samsung Electronics, the world's largest memory chip manufacturer, has experienced an extraordinary financial turnaround, with operating profit surging approximately 18-fold year-over-year to reach record levels in the second quarter. The company's shares have appreciated 158% this year, while SK Hynix shares have gained 273% and Micron shares have risen 242%. All three companies have now achieved market capitalizations exceeding $1 trillion, reflecting investor confidence in the sustained growth trajectory of the AI memory market. Nomura Securities anticipates that commodity DRAM prices will increase 24% quarter-over-quarter and NAND prices will rise 25% in the July through September period, supported by robust demand from both consumer memory products and chips for traditional and AI data centers.

The pricing environment for memory chips has reached levels not seen in years, with Micron reporting that DRAM memory chip prices rose more than 60% in the quarter ended May 28 compared with the previous quarter, while NAND flash memory prices increased more than 80%. These dramatic price increases reflect the growing importance of semiconductor suppliers within the AI supply chain, as chip manufacturers benefit from one of the strongest pricing environments the industry has experienced in decades. The limited manufacturing capacity for HBM chips has kept supply tight as demand continues to grow exponentially, creating a favorable dynamic for memory chip makers who can command premium pricing for their products.

The hyperscaler capital expenditure cycle continues to provide fundamental support for memory chip demand. The world's four largest cloud computing providers are projected to spend more than $700 billion on AI infrastructure this year alone, ensuring that demand remains elevated for the components powering next-generation AI systems. Samsung Group and SK Group have announced plans to build two chipmaking plants each in southwest regions, representing a combined investment of 800 trillion won, as they race to expand manufacturing capacity to meet the insatiable demand for AI memory solutions. These massive capital commitments underscore the industry's confidence in the long-term growth prospects for memory chips, with Bernstein's 2027 timeline aligning with the expected duration of the current AI infrastructure buildout cycle.

The structural drivers behind the memory chip bull market extend beyond immediate AI demand to include broader technological trends. The proliferation of edge computing devices, the expansion of 5G networks, and the increasing sophistication of autonomous vehicles all contribute to growing demand for memory solutions. Data centers continue to expand globally, with each new facility requiring substantial memory capacity to support cloud computing services, artificial intelligence training and inference workloads, and big data analytics applications. The transition to higher-density memory technologies, including DDR5 DRAM and advanced NAND flash architectures, creates additional revenue opportunities for manufacturers as customers upgrade their infrastructure to support higher performance requirements.

However, the memory chip sector has recently experienced significant volatility, with the Roundhill Memory ETF declining 25% from its peak in late June, and individual stocks including SK Hynix and SanDisk falling approximately 28% from their June highs. This correction reflects broader market concerns about the sustainability of AI infrastructure spending and potential supply chain disruptions, rather than any fundamental deterioration in the underlying demand outlook. The sector remains up a median of nearly 60% since late March and has added approximately $5 trillion in market value over that period, indicating that the recent pullback represents a healthy consolidation rather than a trend reversal. Bernstein's prediction that the bull market will continue through 2027 suggests that these corrections should be viewed as buying opportunities rather than signals of a broader market top.

The competitive dynamics within the memory chip industry are also evolving in ways that support sustained profitability. The three dominant players, Samsung, SK Hynix, and Micron, have consolidated market share through years of intense competition that drove weaker competitors from the market. This oligopolistic structure enables disciplined capacity management and rational pricing behavior, reducing the risk of the destructive price wars that characterized earlier periods in the industry's history. The technical complexity of HBM manufacturing creates additional barriers to entry, as new competitors would require years of research and development investment to achieve competitive product yields and performance characteristics.

Investment implications of Bernstein's 2027 bull market prediction are substantial for both equity investors and industry participants. The forecast suggests that memory chip stocks may continue to outperform the broader technology sector, driven by earnings growth that exceeds market expectations. The visibility provided by multi-year contracts and sold-out production capacity reduces uncertainty around future revenue and profitability, supporting higher valuation multiples for memory chip companies. For technology companies dependent on memory components, the extended bull market implies continued cost pressures that may impact margins and necessitate strategic adjustments to procurement and product design strategies.

The geographic concentration of memory chip manufacturing in South Korea and the United States creates strategic considerations for policymakers and investors alike. Government initiatives to support domestic semiconductor production, including the CHIPS Act in the United States and similar programs in other countries, are likely to receive continued funding and political support given the critical importance of memory chips to AI competitiveness and national security. These policy tailwinds provide additional support for the investment case in memory chip companies with significant manufacturing presence in jurisdictions with favorable regulatory environments.

Looking ahead to 2027, the memory chip industry appears well-positioned to maintain its growth trajectory, supported by the continued expansion of AI applications, the proliferation of data-intensive technologies, and the structural supply constraints that limit competitive entry. Bernstein's prediction reflects a comprehensive analysis of demand drivers, competitive dynamics, and supply chain conditions that collectively support an optimistic outlook for the sector. While short-term volatility is inevitable in any cyclical industry, the fundamental underpinnings of the memory chip bull market appear robust enough to sustain the current uptrend for several more years, creating attractive investment opportunities for those with the patience to navigate periodic market fluctuations.

The transformation of memory chips from commodity components to strategic enablers of the AI economy represents a permanent shift in the industry's value proposition. As artificial intelligence continues to permeate every aspect of the global economy, from consumer applications to enterprise software to industrial automation, the demand for high-performance memory solutions will only intensify. Bernstein's prediction that this demand will sustain a bull market through 2027 provides a valuable framework for investors seeking to understand the long-term growth potential of the semiconductor sector and position their portfolios accordingly.@Gate_Square

Bernstein, a leading global investment research and asset management firm, has issued a bold prediction that the memory chip bull market will extend through 2027, driven by unprecedented demand from artificial intelligence infrastructure, data centers, and high-performance computing applications. This forecast represents a significant bullish signal for major memory chip manufacturers including SK Hynix, Samsung Electronics, and Micron Technology, indicating that the current uptrend in the semiconductor sector has substantial runway ahead.

The memory chip industry has experienced a remarkable transformation over the past eighteen months, evolving from a cyclical commodity business into a critical enabler of the AI revolution. High-Bandwidth Memory (HBM) chips have emerged as the most sought-after components in the semiconductor supply chain, with demand significantly outpacing available manufacturing capacity. SK Hynix currently dominates the HBM market with approximately 58% global market share, substantially ahead of Micron's 21% market share. This leadership position has positioned SK Hynix as the primary beneficiary of the AI infrastructure buildout, with Bernstein projecting that the company will achieve gross margins of 91% by the second quarter of 2026, accompanied by operating margins between 70% and 80%. These figures compare favorably to Micron's projected operating margins of 50% to 55%, highlighting SK Hynix's superior competitive positioning in the high-margin HBM segment.

Micron Technology has also demonstrated exceptional performance, with the company reporting record quarterly revenue of $41.46 billion and adjusted gross margins reaching 84.6%. The company has secured approximately $100 billion in contracted multi-year revenue through non-cancelable, take-or-pay agreements, effectively insulating its business from the traditional boom-bust cycles that have historically characterized the DRAM industry. Micron has committed up to $3 billion toward domestic expansion initiatives, including $500 million in strategic financing to GlobalWafers to support its Sherman, Texas facility, alongside a ten-year silicon wafer supply agreement that locks in raw material capacity for the foreseeable future. The company's HBM supply has been completely sold out through 2028, underscoring the structural supply-demand imbalance that continues to drive pricing power across the memory chip sector.

Samsung Electronics, the world's largest memory chip manufacturer, has experienced an extraordinary financial turnaround, with operating profit surging approximately 18-fold year-over-year to reach record levels in the second quarter. The company's shares have appreciated 158% this year, while SK Hynix shares have gained 273% and Micron shares have risen 242%. All three companies have now achieved market capitalizations exceeding $1 trillion, reflecting investor confidence in the sustained growth trajectory of the AI memory market. Nomura Securities anticipates that commodity DRAM prices will increase 24% quarter-over-quarter and NAND prices will rise 25% in the July through September period, supported by robust demand from both consumer memory products and chips for traditional and AI data centers.

The pricing environment for memory chips has reached levels not seen in years, with Micron reporting that DRAM memory chip prices rose more than 60% in the quarter ended May 28 compared with the previous quarter, while NAND flash memory prices increased more than 80%. These dramatic price increases reflect the growing importance of semiconductor suppliers within the AI supply chain, as chip manufacturers benefit from one of the strongest pricing environments the industry has experienced in decades. The limited manufacturing capacity for HBM chips has kept supply tight as demand continues to grow exponentially, creating a favorable dynamic for memory chip makers who can command premium pricing for their products.

The hyperscaler capital expenditure cycle continues to provide fundamental support for memory chip demand. The world's four largest cloud computing providers are projected to spend more than $700 billion on AI infrastructure this year alone, ensuring that demand remains elevated for the components powering next-generation AI systems. Samsung Group and SK Group have announced plans to build two chipmaking plants each in southwest regions, representing a combined investment of 800 trillion won, as they race to expand manufacturing capacity to meet the insatiable demand for AI memory solutions. These massive capital commitments underscore the industry's confidence in the long-term growth prospects for memory chips, with Bernstein's 2027 timeline aligning with the expected duration of the current AI infrastructure buildout cycle.

The structural drivers behind the memory chip bull market extend beyond immediate AI demand to include broader technological trends. The proliferation of edge computing devices, the expansion of 5G networks, and the increasing sophistication of autonomous vehicles all contribute to growing demand for memory solutions. Data centers continue to expand globally, with each new facility requiring substantial memory capacity to support cloud computing services, artificial intelligence training and inference workloads, and big data analytics applications. The transition to higher-density memory technologies, including DDR5 DRAM and advanced NAND flash architectures, creates additional revenue opportunities for manufacturers as customers upgrade their infrastructure to support higher performance requirements.

However, the memory chip sector has recently experienced significant volatility, with the Roundhill Memory ETF declining 25% from its peak in late June, and individual stocks including SK Hynix and SanDisk falling approximately 28% from their June highs. This correction reflects broader market concerns about the sustainability of AI infrastructure spending and potential supply chain disruptions, rather than any fundamental deterioration in the underlying demand outlook. The sector remains up a median of nearly 60% since late March and has added approximately $5 trillion in market value over that period, indicating that the recent pullback represents a healthy consolidation rather than a trend reversal. Bernstein's prediction that the bull market will continue through 2027 suggests that these corrections should be viewed as buying opportunities rather than signals of a broader market top.

The competitive dynamics within the memory chip industry are also evolving in ways that support sustained profitability. The three dominant players, Samsung, SK Hynix, and Micron, have consolidated market share through years of intense competition that drove weaker competitors from the market. This oligopolistic structure enables disciplined capacity management and rational pricing behavior, reducing the risk of the destructive price wars that characterized earlier periods in the industry's history. The technical complexity of HBM manufacturing creates additional barriers to entry, as new competitors would require years of research and development investment to achieve competitive product yields and performance characteristics.

Investment implications of Bernstein's 2027 bull market prediction are substantial for both equity investors and industry participants. The forecast suggests that memory chip stocks may continue to outperform the broader technology sector, driven by earnings growth that exceeds market expectations. The visibility provided by multi-year contracts and sold-out production capacity reduces uncertainty around future revenue and profitability, supporting higher valuation multiples for memory chip companies. For technology companies dependent on memory components, the extended bull market implies continued cost pressures that may impact margins and necessitate strategic adjustments to procurement and product design strategies.

The geographic concentration of memory chip manufacturing in South Korea and the United States creates strategic considerations for policymakers and investors alike. Government initiatives to support domestic semiconductor production, including the CHIPS Act in the United States and similar programs in other countries, are likely to receive continued funding and political support given the critical importance of memory chips to AI competitiveness and national security. These policy tailwinds provide additional support for the investment case in memory chip companies with significant manufacturing presence in jurisdictions with favorable regulatory environments.

Looking ahead to 2027, the memory chip industry appears well-positioned to maintain its growth trajectory, supported by the continued expansion of AI applications, the proliferation of data-intensive technologies, and the structural supply constraints that limit competitive entry. Bernstein's prediction reflects a comprehensive analysis of demand drivers, competitive dynamics, and supply chain conditions that collectively support an optimistic outlook for the sector. While short-term volatility is inevitable in any cyclical industry, the fundamental underpinnings of the memory chip bull market appear robust enough to sustain the current uptrend for several more years, creating attractive investment opportunities for those with the patience to navigate periodic market fluctuations.

The transformation of memory chips from commodity components to strategic enablers of the AI economy represents a permanent shift in the industry's value proposition. As artificial intelligence continues to permeate every aspect of the global economy, from consumer applications to enterprise software to industrial automation, the demand for high-performance memory solutions will only intensify. Bernstein's prediction that this demand will sustain a bull market through 2027 provides a valuable framework for investors seeking to understand the long-term growth potential of the semiconductor sector and position their portfolios accordingly.@Gate_Square